- Key Takeaways

- AI Everywhere, Impact Nowhere

- Inside the Incubator: Where Banks Lose AI Value

- The Six Hidden Value Gaps AI Can Solve in Banking Today

- Two AI Solutions That Consistently Passed Validation

- The Four Failure Patterns Behind AI Projects

- Why Validation Is the New Competitive Edge in Financial Services

- What Banks Don’t Need vs What Banks Do Need

- In Summary: The Path Forward for Fintech Leaders

Key Takeaways

- AI validation is becoming the core advantage in financial services.

- Siloed PoCs drain budgets while producing almost no ROI.

- Inactivity, not onboarding, is where banks lose the most value.

- Banks that validate first and scale second will dominate the next fintech wave.

AI has become the new competitive frontier in financial services, but not in the way most banks expected. The industry’s challenge is no longer AI scarcity but AI saturation. Most large banks and fintech companies now run dozens, even hundreds, of siloed pilots across fraud, risk, underwriting, onboarding, customer engagement, and servicing. According to McKinsey, 88% of financial institutions already use AI somewhere, yet only one-third have scaled it beyond the pilot stage. The AI capability exists, but the outcomes don’t complement. And the gap between ambition and measurable impact is widening fast.

AI Everywhere, Impact Nowhere

Nearly every bank has an AI roadmap, an innovation lab, and a growing portfolio of early-stage projects. Yet few see meaningful ROI. A small subset of institutions convert AI into margin gains and customer engagement uplift, but most see flat outcomes despite millions being poured into projects.

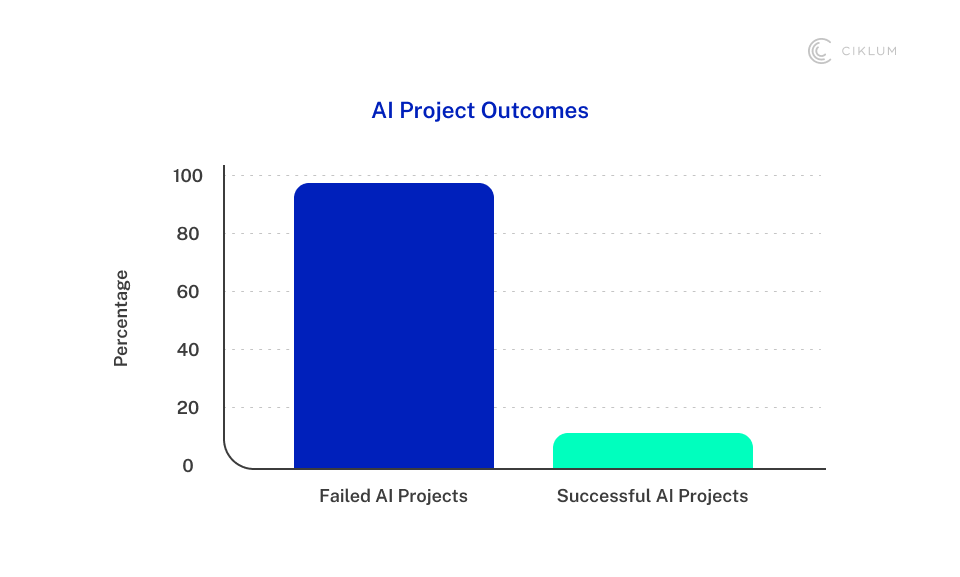

In an environment where real-time decisioning, cross-bank behavioural signals, and event-driven architectures are becoming standard, the banks that fall behind are the ones still guessing what to build. MIT’s ongoing AI Performance Index now shows that 95% of AI pilots fail to create measurable impact, even inside organisations with mature data programs.

This realisation pushed us to run a dedicated AI incubator for financial services, not to generate more ideas, but to filter them. Through months of interviews, journey mapping, and real-world validation across banking teams, we uncovered where AI value genuinely hides in financial services and why most institutions consistently fail to reach it.

Inside the Incubator: Where Banks Lose AI Value

When we began the incubator, nearly every bank believed onboarding was its biggest problem. It’s visible, compliance-heavy, and undeniably costly. But once we dug deeper by mapping customer journeys, examining behavioural data, and running validation cycles, a different picture emerged.

Banks weren’t losing value at the front door. They were losing it in the silent middle.

We uncovered value gaps far larger than onboarding:

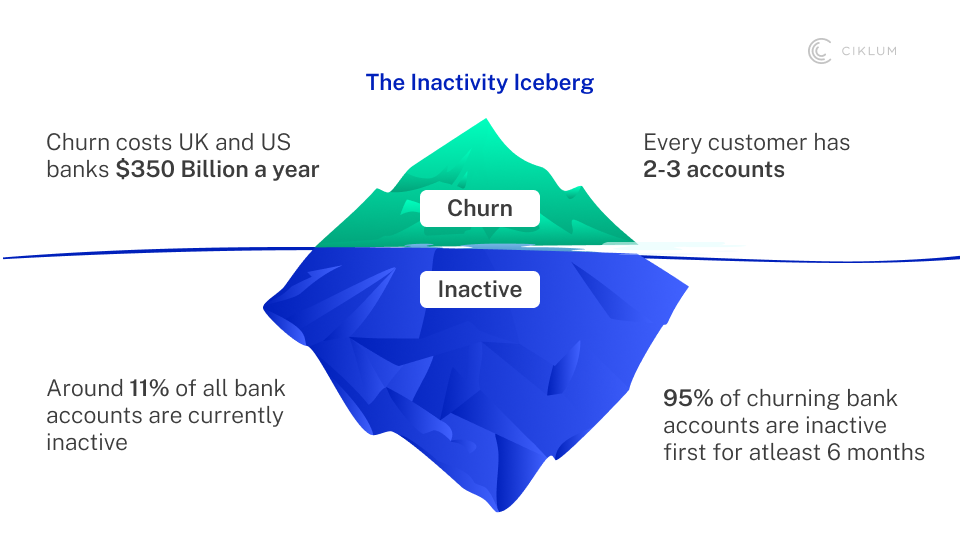

- Massive pools of inactive customers (11% of accounts are inactive at any point)

- Silent churn (95% of churning accounts were inactive for at least 6 months first)

- Low product engagement post-signup

Fragmented experiences for multi-account customers - High-value life moments consistently missed

- Notifications and alerts that customers routinely ignore

The industry spends around £300 to acquire a new customer, but only £60 to retain one. Yet retention, and not acquisition, is where value is leaking at scale. Customers onboarded successfully, then went inactive, disengaged, or silently drifted toward competitors.

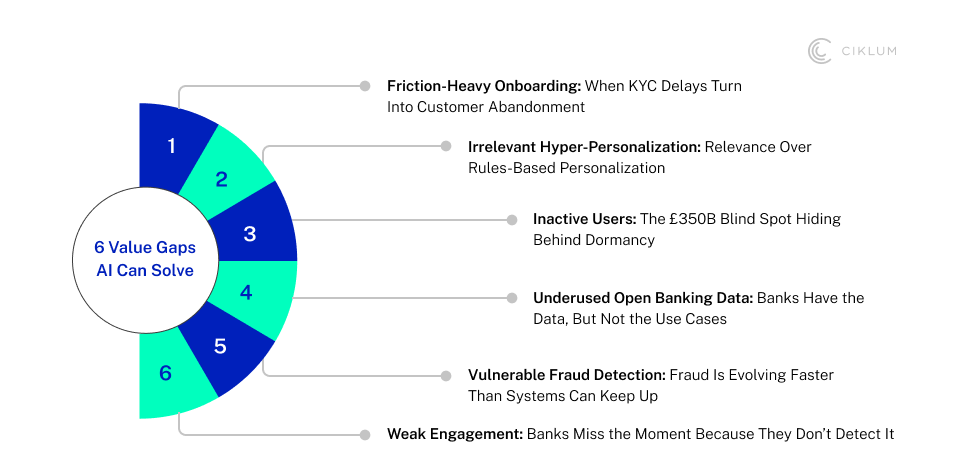

The Six Hidden Value Gaps AI Can Solve in Banking Today

Across financial services, several opportunity areas and everyday problems consistently surface that AI can meaningfully improve right now.

Friction-Heavy Onboarding

60–70% of users abandon digital applications mostly because of slow KYC checks or repeated document uploads. A typical scenario is a customer uploading their ID, waiting for verification, then being asked to upload it again because the system couldn’t read it, leading to instant drop-off and loss of acquisition money. But fast onboarding alone doesn’t fix the deeper issue. Customers who onboard smoothly can still go inactive if engagement breaks later.

Hyper-Personalization That Doesn’t Deliver

While 71% of customers expect personalization and fewer than 20% feel they receive it, most banks still rely on generic, rules-based recommendations. It’s why someone who’s never taken a loan still gets templated loan offers. AI can move banks toward moment-aware personalization, but only if teams validate which signals and life events actually drive relevance.

Inactive or Dormant Users

This is the silent killer. Approximately 25–40% of new users become inactive within 90 days, and inactivity often precedes nearly every subsequent churn event. They don’t leave because products are bad, they leave because no one reaches them with something that matters.

Underused Open Banking Data

Open Banking provides a wealth of cross-account insights, yet only a few banks use this data meaningfully. You’ll see customers with frequent travel-related purchases, but their main bank still sends generic savings prompts instead of FX-fee alerts. AI can convert data into useful intelligence, but only when banks validate which use cases customers actually value.

AI-Driven Fraud Detection That Misses Signals

According to NASDAQ, fraud costs fintechs more than $500 billion annually. But many banks still rely on rigid, rules-based systems. A common scenario is everyday local purchases suddenly followed by a small international test transaction that slips through because the rule engine treats it as low risk, only for several high-value fraudulent charges to follow. AI can improve the quality of anomaly detection by 50%, but it needs to be trained on validated, high-quality signals.

Poor Engagement and Weak Cross-Sell Journeys

Banks still push broad campaigns and generic app banners instead of responding to customer context. Customers travel, shop, invest elsewhere, and their primary bank still sends generic savings prompts. These little missed opportunities turn into timely, high-value engagements.

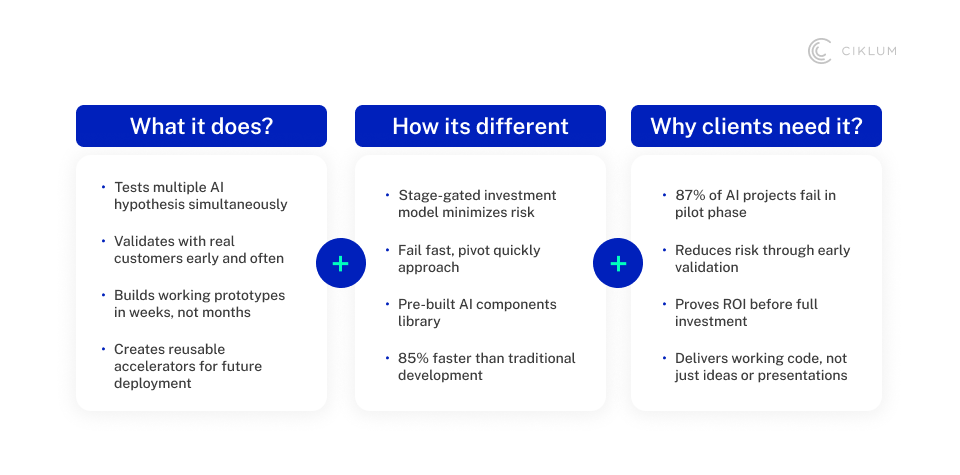

Two AI Solutions That Consistently Passed Validation

We filtered dozens of ideas down to two high-impact, scalable solutions that directly addressed the industry’s biggest gaps.

The AI Re-Engager

Designed to tackle the inactivity iceberg, the AI Re-Engager predicts when customers are likely to disengage, identifies the behaviours behind it, and triggers personalised nudges that restore activity.

The Live Moment Predictor

The Live Moment Predictor identifies the life moments where banks can deliver genuine value, but rarely do. It tracks signals like spending shifts, location changes, travel activity, and major financial behaviours, like moving house, planning travel, or expecting a child. It empowers banks to act proactively and offer help before the customer even asks.

The Four Failure Patterns Behind AI Projects

Across all our conversations and validation cycles, one message was universal: banks don’t fail because of weak ideas, but because of weak validation.

Here are the five patterns we saw repeatedly:

Feature Sprawl

Banks often build too many features into a product at once. Teams launch new features, add AI-powered widgets, or experiment with models before proving whether customers actually want any of it.

Hype-Led Use Cases

GenAI and LLMs dominate every conversation today, and banks feel pressure to “do something” with them. But when technology becomes the starting point instead of the problem, teams end up chasing hype instead of customer pain points.

Siloed Teams

Data, product, engineering, and compliance validate separately, creating conflicting priorities and slow cycles.

No Validation Framework

Workshops and interviews aren’t validation. Real validation requires behavioural evidence, customer signals, and measurable proof of value.

Why Validation Is the New Competitive Edge in Financial Services

When you look at why most AI initiatives stall, the obvious pattern is that banks are investing in the wrong things. The institutions that turn AI into tangible business outcomes focus less on building more and more on validation, and then build the right thing. In simple terms, the banks that win with AI prioritise precision over volume. The shift looks like this:

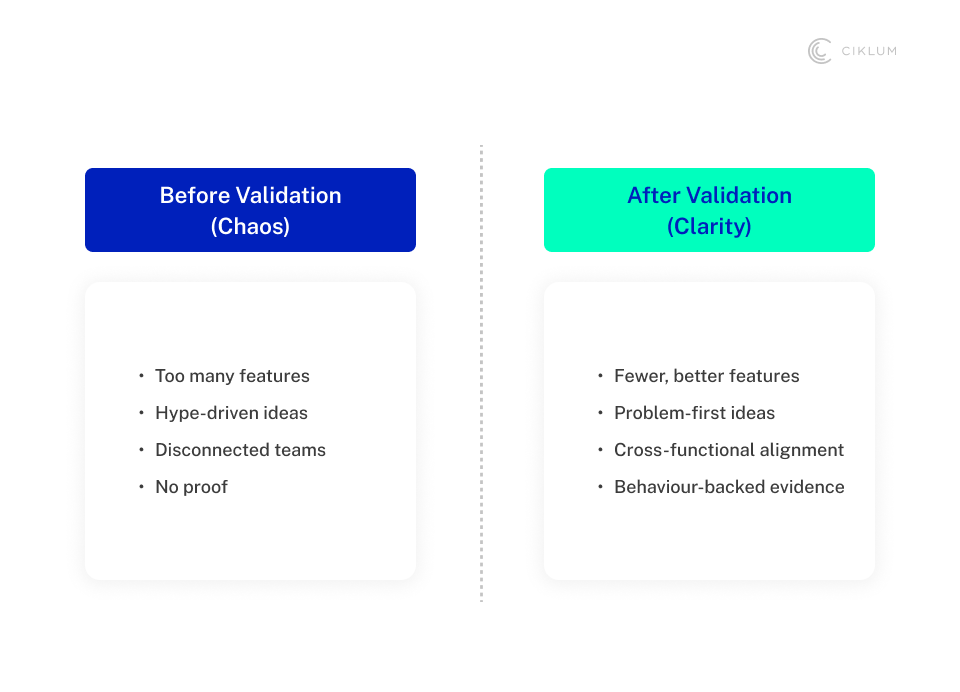

What Banks Don’t Need vs What Banks Do Need

| What Banks Don’t Need | What Banks Do Need |

| More AI PoCs and experiments | A disciplined, repeatable validation framework |

| More vendor demos or tech showcases | A clear view of where value sits across the customer lifecycle |

| More features added to already complex products | Fewer, better features validated against real customer behaviour |

| Hype-driven use cases (GenAI for the sake of it) | Problem-first design anchored in measurable business outcomes |

| Siloed team decision-making | Cross-functional alignment between data, product, engineering, and compliance |

| Assumptions about what customers want | Evidence, behavioural insights, and user-level validation |

In Summary: The Path Forward for Fintech Leaders

If 2025 was the year of experimenting with AI, 2026 will be the year of proving what works. Our work shows exactly where banks lose value and where they can gain it back. And that’s by validating the right problems early and scaling AI with precision. The winners will be the institutions that treat validation as a capability, not a checkbox.

That’s the message we’re taking to Fintech Connect, and it's the philosophy that shapes how Ciklum helps financial services leaders move from pilots to performance. If these insights resonate and you're exploring how to unlock the true value of AI, we’d love to continue the conversation.

By Ivana Veljovic

Senior Product Manager

Ivana Veljovic is part of Ciklum’s Experience team, where she brings product, engineering, and design together to ensure solutions are validated early and built for real value.

Blogs

Discover Similar Insights

From AI Interest to Engineering-Ready Mandates: Why The Market Needs AI Clinics, Not More AI Pilots

Learn More

Agentification of Payments: A Strategic Shift for PSPs

Learn More

Explainable AI in Banking: Designing Transparent, Auditable Models for Credit, Risk, and Compliance

Learn More

Payments Without Friction: Modern Checkout Is Your Competitive Edge

Learn More