- Key Takeaways

- How AI Is Reshaping Contact Centres in Banking and Financial Services

- What Is an Agentic AI Contact Centre? (And Why It Matters for Banks)

- AI Call Centre Use Cases in Banking: What's Working in 2026

- AI Contact Centre Compliance: How to Meet Financial Services Regulatory Requirements

- The Technology Stack Behind a Compliant AI Call Centre

- AI Call Centre for Banking: Key Takeaways and Next Steps

By Sarah Topping, Ciklum & Jerry Haywood, boost.ai

In partnership: Ciklum × boost.ai

Key Takeaways

- Banking customers prefer voice contact — but traditional models make it prohibitively expensive to scale

- AI call centre technology for banking and financial services is now production-ready

- Agentic AI contact centre solutions autonomously handle high-volume use cases — from fraud alerts and KYC to loan servicing

- Compliance-by-design, including FCA Consumer Duty, MiFID II, and UK GDPR, can be built in from the outset

Voice has never gone away in banking and financial services — but the economics behind it are increasingly unsustainable. While digital channels have scaled, complex, high-value interactions still default to voice, where cost-to-serve is highest, and experience is most inconsistent.

This creates a structural challenge: organisations cannot remove voice, but they cannot scale it efficiently using traditional models.

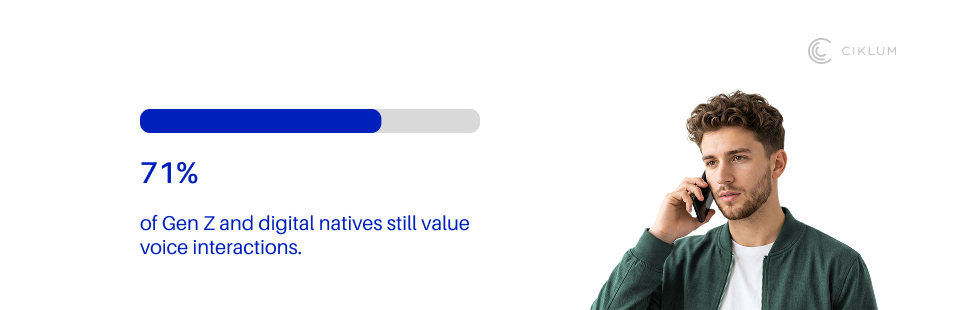

This is reinforced by changing customer expectations. Research shows that even digitally native customers, including Gen Z, increasingly expect natural, real-time voice interactions when resolving complex issues, rather than navigating fragmented digital journeys. In fact, 71% highlighted that voice remains a critical channel even for the most digitally fluent users.

Of course, in practice, hiring enough customer service agents to field all customer service calls quickly and effectively can be financially prohibitive for many businesses. And this is where AI call centre technology can deliver the best of both worlds: personalised contact for customers and more cost-effective customer service operations for the business.

In this blog, we'll explore what AI in contact centre operations looks like across banking and financial services, including the key use cases it can be applied to, and why it's important to consider risk and governance from the outset.

How AI Is Reshaping Contact Centres in Banking and Financial Services

Traditional contact center models force a trade-off between cost and experience. Human-led voice delivers quality but does not scale efficiently, while IVR and legacy automation reduce cost but degrade experience.

This is where contact center AI and contact center automation begin to change the economics, giving banks a way to resolve more calls without simply adding more agents.

To understand what changes this dynamic, an agentic voice system understands what a customer is trying to achieve, takes autonomous steps to resolve it (checking accounts, verifying identity, updating records), and escalates to a human only when genuinely needed.

In plain English, we’re talking about goal-driven AI. It can hold a conversation, access the right systems, follow approved workflows, and take action on the customer’s behalf. For banks, this matters because many customer queries are not especially complex. They are just high-volume, repetitive, and operationally expensive.

Balance checks, card blocks, document reminders, loan status updates, fraud alerts, and KYC checks do not always require a senior human agent. What they do require is speed, accuracy, secure system access, and a clear audit trail.

This has led many organisations to embrace the possibilities of generative AI in contact center automation to handle customer service queries at much greater scale and much lower cost.

Some recent credible industry thought leaders also have the same viewpoint.

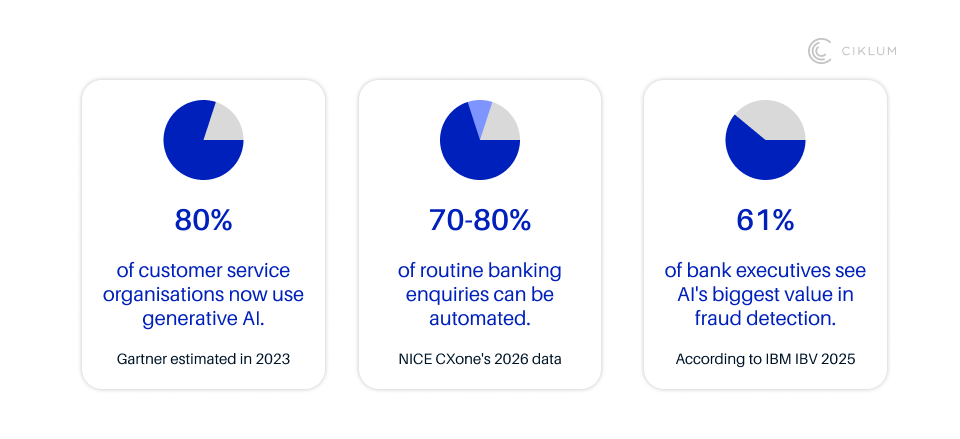

- Gartner estimated in 2023 that as many as 80% of customer service and support organisations are now using generative AI, either to boost customer experience or aid agent productivity.

- NICE CXone's 2026 data shows that 70–80% of routine banking and financial services enquiries can now be resolved without human intervention.

- And according to IBM IBV 2025, 61% of bank executives identify fraud risk detection as AI's biggest business value driver — making the contact centre a direct line to financial crime prevention.

For years, automation often came at the expense of voice-based interaction, leaving customers frustrated when they could not explain a complex issue naturally. AI has not been able to solve that problem properly until now.

Jerry Haywood, CEO of boost.ai, notes that this shift is fundamentally about business logic, not just technology. boost.ai is a conversational AI platform purpose-built for regulated industries, deployed across major Scandinavian and European banks — including institutions operating under FCA and PRA oversight.

"Legacy IVRs were built for containment, not resolution — and customers feel that friction every time they call.

In banking, voice is where the highest-stakes conversations happen, but scaling it has always meant a trade-off between service and cost. That's changing. We're moving beyond rigid menus to boost.ai agents that understand intent and take action — from fraud alerts to complex servicing.

The result is high-touch service at a scale that's finally sustainable — and a reset for what great voice experiences should feel like."

What Is an Agentic AI Contact Centre? (And Why It Matters for Banks)

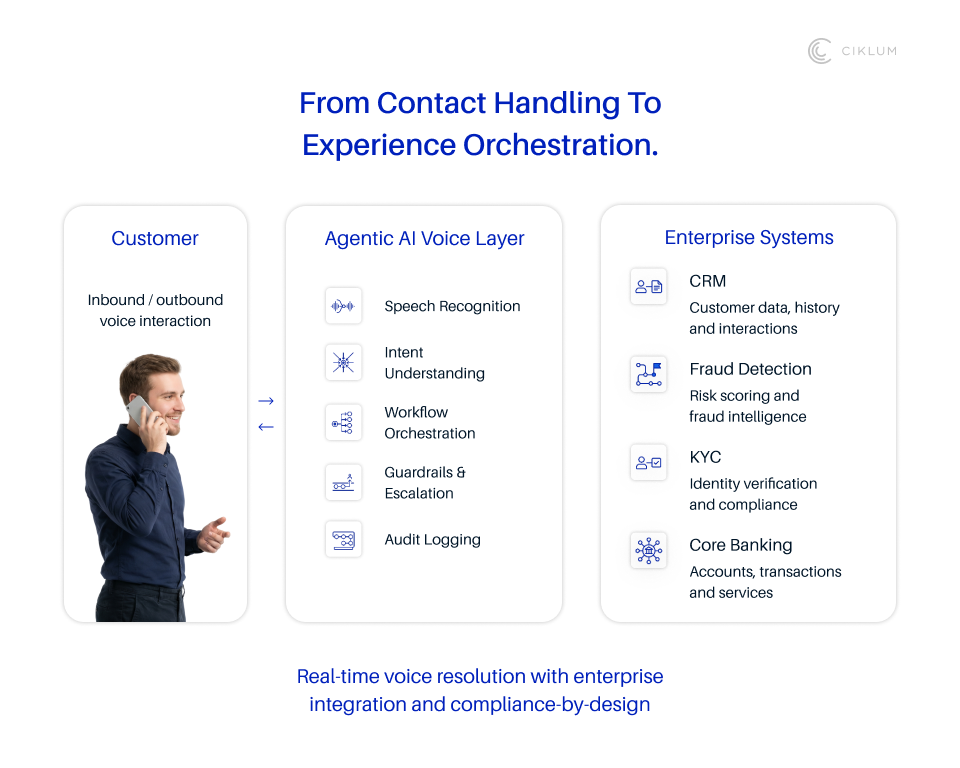

An agentic AI contact centre goes beyond conversational AI. It does not simply respond, it acts. It combines real-time speech recognition, large language models, and orchestration frameworks to:

- Understand customer intent in context

- Determine the appropriate action or workflow

- Execute tasks across backend systems

- Apply guardrails, compliance rules, and escalation logic

This transforms voice from a reactive channel into an execution layer for customer operations.

To make this real, imagine a customer calls their bank because they have spotted a suspicious transaction on their current account. Instead of waiting in a queue and repeating details, the AI understands the issue immediately. It checks the fraud system, verifies the customer through voice biometrics, removes the block where appropriate, and records the full interaction for FCA compliance.

All of this happens in under 90 seconds, without a human agent needing to step in.

The difference between this and a traditional IVR is not one of degree, but one of purpose. A traditional IVR is built to manage the call: routing, menus, deflection. An AI call centre is built to resolve the issue: understanding intent, accessing systems, and completing the transaction. For a regulated UK financial institution, this distinction matters beyond customer experience. If a customer cannot resolve a blocked card, suspicious transaction, or fraud alert through voice, the risk simply moves downstream.

AI Call Centre Use Cases in Banking: What's Working in 2026

Agentic AI contact centres are redefining how the contact centre operates within a bank or financial services firm. No longer is it a human-led operation supported by a simple voicebot. Instead, the contact centre becomes an integrated ecosystem of goal-directed AI agents working alongside humans.

Fraud Alerts & Card Disputes

When a customer's card is blocked or a suspicious transaction is flagged, the instinctive response is to call — not to open an app or start a live chat. AI voice's ability to handle fraud alerts with identity verification at scale is uniquely powerful in the banking context, where fraud losses in the UK hit over £1.1 billion in 2024.

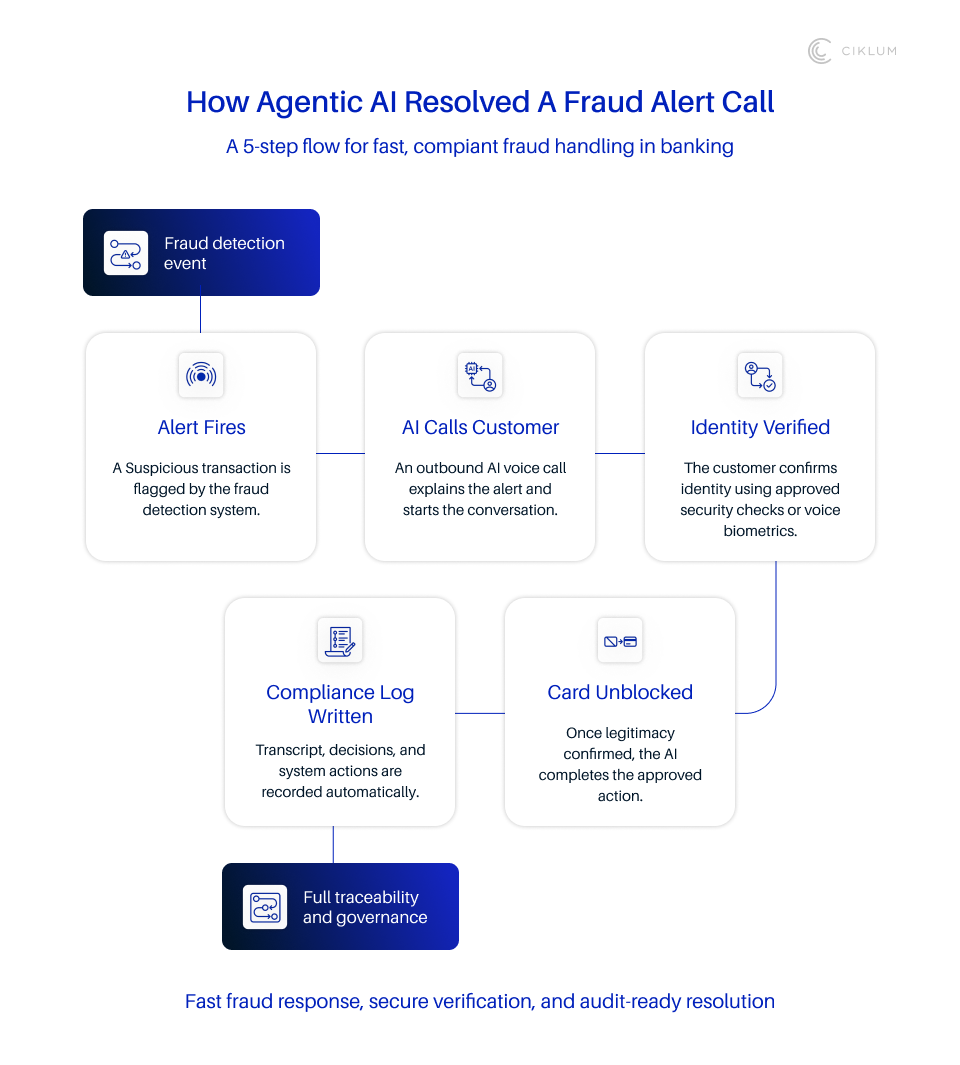

Here is how an agentic AI handles a fraud alert call end-to-end:

Alert fires: The fraud detection system flags a suspicious transaction and triggers an outbound AI voice call.

Alert fires: The fraud detection system flags a suspicious transaction and triggers an outbound AI voice call. AI calls customer: The AI voice agent contacts the customer, explains the alert, and starts identity verification.

AI calls customer: The AI voice agent contacts the customer, explains the alert, and starts identity verification. Identity verified: The customer confirms their identity via security questions or voice biometrics

Identity verified: The customer confirms their identity via security questions or voice biometrics Card unblocked or confirmed blocked: Based on the customer's response, the AI resolves the issue or escalates to a human agent.

Card unblocked or confirmed blocked: Based on the customer's response, the AI resolves the issue or escalates to a human agent. Compliance log written: The full interaction is recorded automatically for FCA and MiFID II compliance purposes.

Compliance log written: The full interaction is recorded automatically for FCA and MiFID II compliance purposes.

KYC & Onboarding

AI voice agents can guide customers through Know Your Customer (KYC) identity verification and account opening flows, collecting the required documentation consent and data while maintaining a full audit trail that satisfies FCA and AML obligations.

Loan & Mortgage Servicing

Loan status updates, document collection, and debt restructuring conversations can be handled at scale, with deterministic workflow logic ensuring every interaction stays within regulatory boundaries.

Routine Account Queries

Balance enquiries, card management, transaction disputes, and payment queries represent the highest-volume, lowest-complexity call types, and the first candidates for AI voice resolution in most banking environments.

The common thread across all these use cases is that they are low or medium in complexity and high in volume. This means the gains — in both customer experience and operational efficiency — can drive a considerable ROI.

According to a ContactBabel report, the average cost of an inbound call in the UK is £5.58. For complex banking interactions, that figure climbs significantly higher. AI contact centre solutions can bring the cost of routine interactions to £0.40–1.50 per resolved query. Combined with containment rate improvements, the ROI case typically closes within 12–18 months of full production rollout.

AI contact centre deployments perform best where workflows are well-defined, decisions are auditable, and outcomes can be governed.

AI Contact Centre Compliance: How to Meet Financial Services Regulatory Requirements

As banking and financial services is one of the most heavily regulated sectors, ensuring that AI works reliably, responsibly, and safely has to be a top priority.

Even though the technology behind agentic AI has come on leaps and bounds in recent years, there are still several potential issues to address, such as:

- AI Failure Modes: In voice-based systems, risks typically arise from three areas: speech recognition errors, intent misclassification, or AI-generated inaccuracies. These risks are mitigated through deterministic workflows, clear decision boundaries, and human-in-the-loop oversight to ensure actions remain controlled and auditable.

- Bias: Controls and workflows help reduce the risk of biased response patterns based on customer speech or behaviour. This is especially important for diverse UK communities, including regional accents, non-English-first speakers, and elderly customers who rely on voice as primary channel.

- Data Privacy: Given the sensitivity of the information involved, including personal and financial data, it’s imperative that AI agents can only use information for its stated purpose. Redacting personally identifiable information (PII) from AI agents can ensure that this information cannot be re-used by the model in the future.

- Regulatory Scrutiny: Scrutiny from regulators is understandably close. Full interaction traces are essential for demonstrating transparency and responsible AI activity.

A compliant AI call centre built for banking and financial services must address five core regulatory expectations:

| Regulation | What it means for banking and financial services | How the AI call centre supports it |

| FCA Consumer Duty | Customers must receive clear support, fair outcomes, and timely escalation where needed. | Logs each interaction, tracks decision points, and escalates vulnerable or complex cases to a human agent. |

| MiFID II | Relevant financial conversations must be recorded, retained, and auditable. | Records calls, transcripts, metadata, and system actions for compliance review. |

| UK GDPR | Customer voice data, personal data, and consent must be handled securely. | Captures consent, masks PII, limits data use, and protects sensitive customer information. |

| AML / KYC | Identity checks and suspicious activity processes must be structured and consistent. | Guides customers through approved verification flows and flags cases requiring review. |

| FCA SYSC | Critical services must remain controlled, resilient, and operationally monitored. | Uses failover logic, escalation paths, audit trails, and monitoring to reduce operational risk. |

The Technology Stack Behind a Compliant AI Call Centre

For banking and financial services organisations navigating these risks, a Hybrid AI architecture is the recommended approach, especially when evaluating AI contact center solutions that need to balance fluency, control, and compliance.

Rather than relying solely on large language models, the most resilient systems combine LLMs with Natural Language Understanding to balance conversational fluency with deterministic logic.

Natural Language Understanding (NLU) for Voice

NLU interprets the many different ways customers describe the same intent. Whether a customer says "I think someone might have misused my card" or "there's a dodgy transaction on my bank statement," the system maps both to the same fraud-alert workflow. Platforms like boost.ai differentiate this from generic voice AI: NLU purpose-built for banking vocabulary, UK regional accents, and regulated service scenarios.

Real-Time System Integration

High-stakes actions, which includes transaction processing and identity verification, are tethered to rule-based flows with defined decision points. This integration layer connects the AI voice agent directly to core banking systems, CRM, fraud detection, and document management platforms in real time.

Compliance & Audit Layer

At the architecture level, the AI agent is built with clear guardrails around what it can receive, say, and do. Sensitive personal information is masked, approved boundaries are enforced, and the agent cannot operate outside the compliance rules set for it.

AI Call Centre for Banking: Key Takeaways and Next Steps

Agentic AI voice represents a fundamental shift in how contact centres operate. For financial services organisations, this is an opportunity to redesign customer operations around speed, accuracy, and scalability, while maintaining the governance required in regulated environments.

In that sense, financial services AI is not only about automation. It is about creating safer, faster, and more auditable customer journeys.

For teams at UK banks and insurers evaluating AI banking solutions, a realistic implementation path looks like this:

- FCA/compliance scoping (4–6 weeks): Map call types against regulatory requirements; identify FCA Consumer Duty, MiFID II, and UK GDPR obligations per use case.

- Integration design (4–8 weeks): Define system integration architecture — core banking, CRM, fraud detection, identity verification.

- Pilot (6–12 weeks): Deploy with a single use case — typically balance enquiries or fraud alerts, with full compliance logging active from day one.

- Production rollout: Expand to additional use cases with the compliance-by-design framework already in place.

The organisations that succeed will not be those that simply deploy AI voice. They will be those that embed it into well-defined workflows, compliant architecture, and clear operating models.

Start here: a three-step framework for UK financial services teams

- Map your top five call types by volume and complexity. These are your AI call centre candidates.

- Identify which FCA, PRA, and AML regulatory requirements apply per call type.

- Pilot with one use case before expanding, with compliance logging active from day one.

UK banks should also ensure voice AI performs across regional accents and diverse customer groups, including Scottish, Welsh, Geordie, South Asian, non-English-first, and elderly callers. A banking-grade AI call centre must prove it can serve this range reliably. Platforms like boost.ai are built and tested against this range.

Now is the time to begin your journey towards an AI call centre for banking, if your organisation has not already done so. Together, Ciklum and boost.ai bring the capabilities needed to turn this vision into a live, compliant solution – combining Ciklum's engineering and orchestration expertise with boost.ai's conversational AI voice interaction engine to deliver secure, scalable AI call centre technology for banking and financial services.

To find out more about the technical steps on the road to a live, compliant voice contact centre (one that works for your customers and your business) take a look at this guide on contact centre execution for financial services leaders.

By Sarah Topping

Principal Lead - Intelligent Automation & Conversational AI

Sarah leads Conversational AI at Ciklum, spearheading AI-powered transformations in retail, publishing, and automotive. With a decade of experience, she develops award-winning virtual assistants and champions Responsible AI to enhance user experiences and operational efficiency.

Blogs

Discover Similar Insights

Agentic AI in Retail: Closing the Gap Between Customer Intent and Enterprise Systems

Learn More

Enterprise AI Automation: A Practical Guide to GenAI, AI Agents and Intelligent Workflows

Learn More

Connecting AI to Your Business: A Complete Guide to MCP Servers

Learn More

From Copilot to Operating Model: What Agentic AI Changes in 2026

Learn More