- Key takeaways:

- Payments Are About to Change - Again.

- From Orchestration to Agentification

- What Agentification Means for PSPs

- ACP and AP2: The Protocols Shaping Agent‑Driven Payments

- How This Changes the PSP’s Game

- What PSPs Should Do Now: The Strategic Moves That Matter

- How Ciklum Helps PSPs Move from Concept to Production

- Build What Agents Will Actually Use

Key takeaways:

- Agentification shifts payments to AI-initiated API calls, bypassing UI for PSPs.

- Core needs: mandates, KYAI, agent tokenization, and real-time risk.

- Adopt ACP (Stripe/OpenAI) and AP2 (Google) protocols for interoperability.

- PSPs must segment agent traffic, pick stack roles, and scale experiments fast.

Payments Are About to Change - Again.

Payment service providers (PSPs) have spent years perfecting payment orchestration: routing transactions across gateways, acquirers, and payment methods to improve approvals, reduce costs, and smooth checkout.

Now, a new shift is underway - one that changes not just how payments are routed, but who initiates them.

AI agents are starting to handle buying and payments autonomously, on behalf of users. That’s not just automation; it’s agentification of payments - a world where software, not humans, becomes the primary “buyer.”

For PSPs, this is not a nice‑to‑have trend. It’s a strategic inflection point that touches every core challenge you already face: compliance, fraud, complexity, and competition.

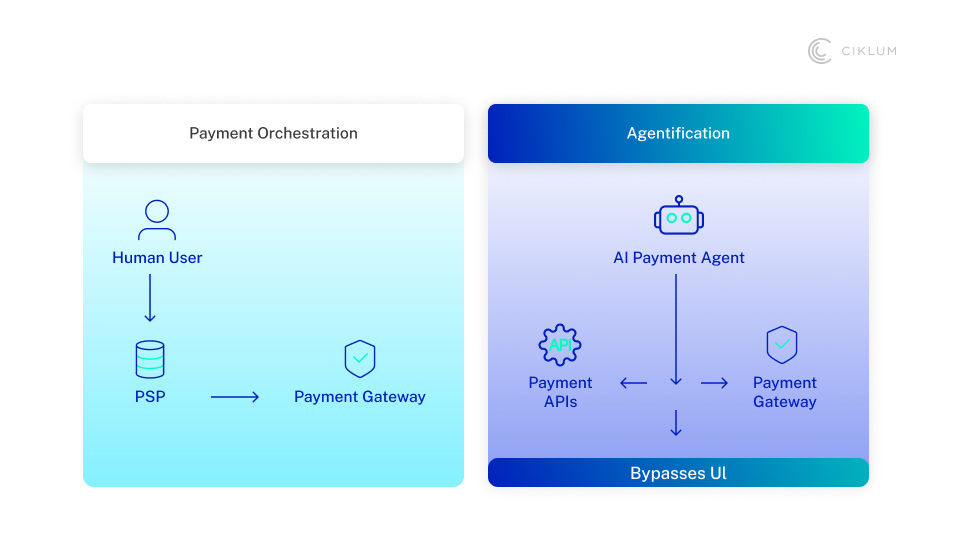

From Orchestration to Agentification

Traditional payment orchestration is about connecting PSPs, rails, and rules. Agents sit on top of that stack, but they’re not the core focus.

Agentification flips the perspective:

- Instead of “how do we route payments better?” the question becomes “how do we embed ourselves into agent‑driven commerce?”

- Instead of orchestrating PSPs, PSPs must orchestrate trust, identity, and permissions for agents.

In this world, the “buyer” is no longer a person clicking a button. It’s an AI agent acting on behalf of a user, interacting directly with payment APIs. The checkout UI disappears; the payment experience becomes invisible.

For PSPs, that means:

- The value is no longer in the button - it’s in the infrastructure behind it.

- The risk is no longer just fraud - it’s also unauthorized agent behavior and consent drift.

What Agentification Means for PSPs

Agentification changes the nature of payment initiation, and, by extension, the PSP’s role in the ecosystem.

1. The “Pay” button becomes an API call

AI agents don’t fill out forms or type card details. They call payment APIs directly.

That means:

- The traditional checkout flow is bypassed.

- The user experience is abstracted away, and the PSP becomes a backend enabler, not a frontend feature.

PSPs that remain only as processors risk becoming invisible. Those that become agent‑ready infrastructure providers will be central to every transaction.

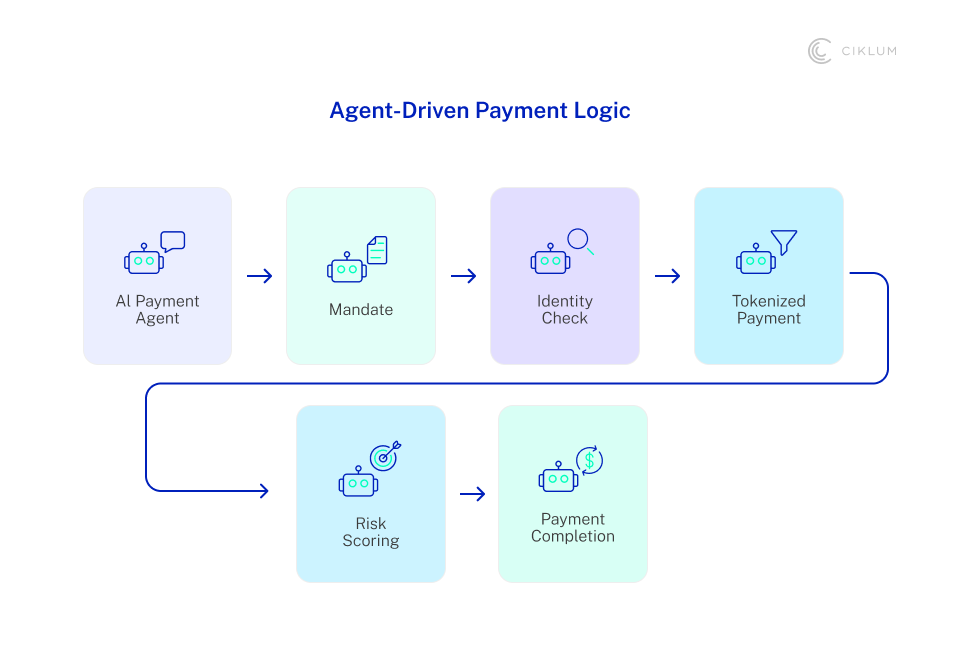

2. Consent and control move to machine‑readable mandates

In agent‑driven commerce, users won’t be present at every payment. Instead, they grant machine‑readable mandates - digital permissions that define what an agent can do.

These can include:

- Spend limits.

- Merchant categories.

- Time windows.

- Risk tolerance.

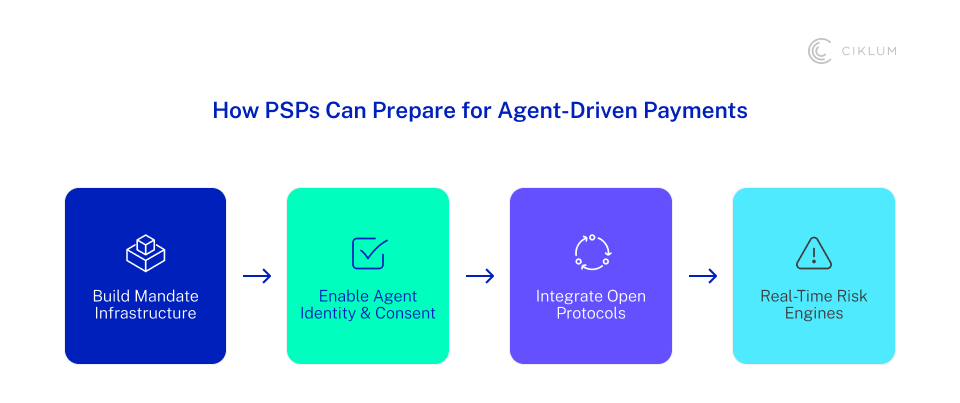

For PSPs, this means building mandate management as a core capability, not an add‑on.

3. Identity shifts from “Know Your Customer” to “Know Your Agent’s Intent” (KYAI)

KYC/AML is no longer enough. PSPs must also understand who the agent is and what it’s allowed to do.

This is where KYA/KYAI (Know Your Agent / Know Your Agent’s Intent) comes in:

- Verifying who built the agent and who owns it.

- Defining what the agent is allowed to do (spend limits, merchant categories, time windows).

- Creating an audit trail so disputes and chargebacks can be traced back to user‑signed mandates.

For PSPs, this means:

- Building agent identity registries or integrating with third‑party KYA services.

- Supporting verifiable credentials and delegated authorization ledgers.

- Treating agent‑initiated transactions as a distinct risk and compliance class, not just “another API call.”

4. Tokenization becomes the new front line

Agents should never see raw payment instruments. Instead, they should transact through tokens, vaults, and escrow services.

This means:

- PSPs must expand tokenization beyond card‑on‑file to agent‑on‑file.

- Vaults must evolve into self‑updating security systems that manage token lifecycles dynamically.

In this world, security is not a sidecar - it’s baked into every agent‑initiated payment.

5. Risk and compliance must be real‑time and adaptive

Fraud engines can’t rely on static rules anymore. Agent‑driven payments require real‑time risk scoring, adaptive rule evaluation, and reputation‑based checks.

PSPs must:

- Embed risk and compliance hooks directly into agent‑facing APIs.

- Enable dynamic failover and recovery that agents can trigger autonomously.

The goal is not just to detect fraud, but to enable safe autonomy.

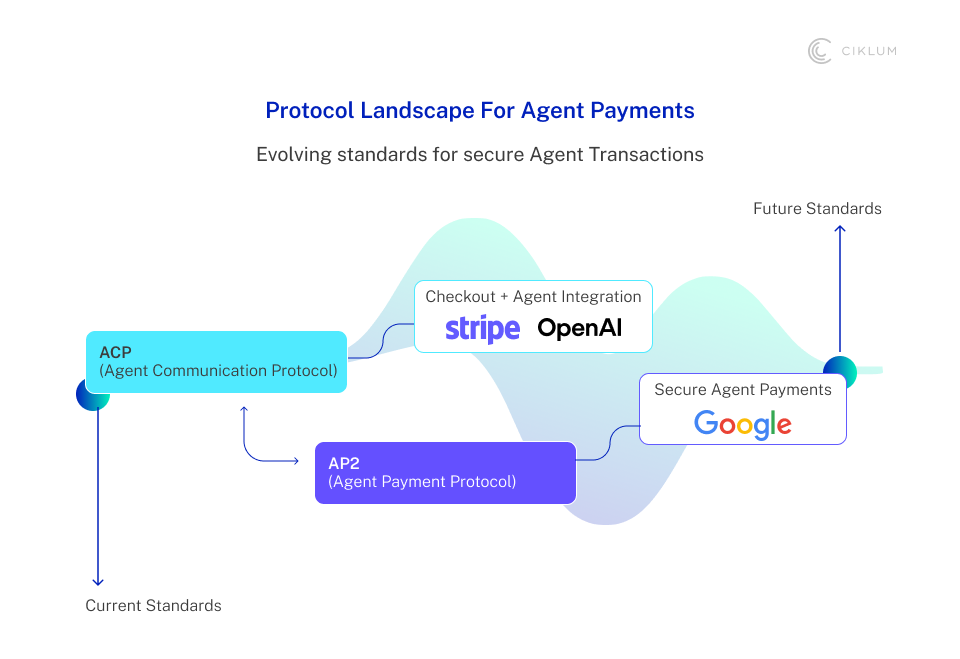

ACP and AP2: The Protocols Shaping Agent‑Driven Payments

Two open protocols are already defining how agents interact with payment systems: ACP (Agentic Commerce Protocol) and AP2 (Agent Payments Protocol).

Agentic Commerce Protocol (ACP) – Stripe & OpenAI

ACP is an open standard that enables programmatic commerce flows between buyers, AI agents, and businesses.

Key points for PSPs:

- It’s designed so merchants can build once and connect to any ACP‑compatible agent (e.g., ChatGPT, other AI assistants).

- It handles secure credential sharing, checkout coordination, and flexible flows (physical goods, subscriptions, asynchronous purchases).

- For PSPs, ACP is a signal that agent‑ready checkout must be standardized, not bespoke.

Agent Payments Protocol (AP2) – Google & partners

AP2 is an open protocol that enables gen‑AI agents to make payments on behalf of users across platforms, with a focus on security, decentralization, and privacy.

Key points:

- AP2 builds on A2A (Agent‑to‑Agent) and aims to be cross‑platform and cross‑rail.

- It emphasizes cryptographic proof of user intent and minimal data exposure.

For PSPs, AP2 suggests:

- The future “Pay” button will be protocol‑agnostic, not platform‑locked.

- PSPs must support multiple agent‑payment standards (ACP, AP2, and others) through flexible APIs and adapters.

How This Changes the PSP’s Game

Taken together, KYA/KYAI, ACP, and AP2 point to a clear shift:

- Identity is no longer just about the human user; it’s about the agent and its mandate.

- Standards are no longer optional; PSPs must support open, interoperable protocols or risk being excluded from agent‑driven flows.

- Risk and compliance must be agent‑aware, with real‑time hooks for consent, limits, and reputation.

For PSPs, the question is no longer “Do we support agents?” but “How deeply do we embed ourselves into these emerging frameworks?”

What PSPs Should Do Now: The Strategic Moves That Matter

At this stage, most PSPs already understand the implications of agent‑driven commerce. The gap is not awareness - it’s execution. The winners will be those who make deliberate architectural and organizational choices in the next months.

Three decisions will define relevance in an agentified payments ecosystem:

1. Decide where you sit in the agent stack

PSPs must explicitly choose their role:

- Execution‑only processor (high volume, low differentiation), or

- Agent trust and orchestration layer (mandates, identity, risk, compliance, recovery).

Trying to sit in both camps without architectural clarity will lead to fragmented platforms and stalled initiatives.

2. Separate “agent traffic” from human traffic

Agent‑initiated payments are not just another API consumer.

They require:

- Distinct consent models.

- Dedicated risk profiles.

- Separate observability and audit layers.

PSPs that fail to segment agent flows early will struggle to scale safely later.

3. Industrialize experimentation - fast

Agentification cannot be solved through one‑off pilots.

PSPs need:

- Controlled sandboxes for agent‑initiated payments.

- Rapid validation of KYAI, mandates, and token models.

- Clear kill/scale decisions tied to business KPIs.

This demands a repeatable innovation mechanism, not ad‑hoc PoCs.

How Ciklum Helps PSPs Move from Concept to Production

We help PSPs design, test, and operationalize agent‑ready payment capabilities using proven engineering and AI‑delivery models.

1. Prodigy: Ciklum’s AI platform & methodology, built on proprietary accelerators, designed to turn enterprise AI vision into production-ready reality. For PSPs ready to build or modernize their core platforms. At the heart of PRODIGY is a platform of proprietary accelerators - Ciklum’s growing library of agents, knowledge engines, and technical building blocks. This IP transforms every solution from a generic AI implementation into a distinct, competitive capability.

What we engineer:

- Modular payment orchestration layers that support both human and agent‑initiated flows.

- Mandate engines and delegated authorization services.

- Tokenization frameworks designed for agent‑on‑file scenarios.

Outcome: Production‑grade platforms that scale across rails, regions, and agent ecosystems.

2. Trust, Risk & Compliance Automation

Agent autonomy only works if trust is machine‑verifiable and real‑time. We help PSPs implement:

- KYAI frameworks and agent identity registries.

- Real‑time risk scoring tailored to agent behavior.

- Audit‑ready consent and mandate traceability.

Outcome: Lower fraud exposure, faster approvals, and regulator‑ready transparency.

4. Platform & Ecosystem Enablement

Agentification is not a single‑vendor game. Ciklum helps PSPs:

- Integrate with ACP, AP2, and emerging agent standards.

- Build protocol‑agnostic adapters instead of brittle custom integrations.

- Partner effectively with AI platforms, networks, and merchants.

Outcome: Future‑proof interoperability without platform lock‑in.

Build What Agents Will Actually Use

Agentification is already reshaping how payments are initiated, authorized, and disputed.

The question for PSPs is no longer if—but how fast and how deliberately you respond.

Work with Ciklum to:

- Pressure‑test your current payment stack against agent‑driven use cases.

- Design an agent‑ready architecture grounded in real standards (ACP, AP2, KYAI).

- Move from fragmented pilots to a scalable, compliant production model.

The future of payments won’t wait for perfect clarity. It will reward those who build early - and build correctly.

By Aaron Jones

Global Head of Product & Experience

Aaron Jones is the Global Head of Product & Experience at Ciklum, where he drives the strategic vision for transitioning ambitious concepts into market-defining products that deliver measurable business impact. He also directs the global Experience Service Line, leading a team of several hundred product and experience practitioners worldwide.

Blogs

Discover Similar Insights

Agentic AI in Retail: Closing the Gap Between Customer Intent and Enterprise Systems

Learn More

From AI Interest to Engineering-Ready Mandates: Why The Market Needs AI Clinics, Not More AI Pilots

Learn More

Explainable AI in Banking: Designing Transparent, Auditable Models for Credit, Risk, and Compliance

Learn More

Payments Without Friction: Modern Checkout Is Your Competitive Edge

Learn More