- Three fronts, one architecture: Leading banks now automate compliance, fraud, and CX together, not as siloed projects. Results come from a shared tech foundation, not separate stacks.

- Shared foundation: Compliance and fraud prevention need the same core: ingesting unstructured data, contextual rules, and auditability. Reducing manual back-office work also boosts customer experience.

- Pilot-to-production gap: Fewer than 10% of banks have GenAI in live use. The main hurdles are operational (data, integration, and governance) not technology.

- Cost and risk are one problem: Manual workflows for compliance and fraud are costly and risky. AI automation lowers both but only if data, orchestration, and governance are built together from day one.

Financial services sit at an unusual intersection. Regulators demand more controls. Fraud is getting more sophisticated. Customers expect faster, more personalized service. These three pressures push in different directions, and most institutions try to address them with separate teams, separate budgets, and separate technology stacks.

BFS organizations advancing in AI automation are recognizing a key insight: compliance, fraud prevention, and customer experience rely on far more shared infrastructure than separate systems suggest.

The same data pipelines that power fraud detection models can also generate compliance reports. The same document processing capabilities that accelerate mortgage approvals can enhance customer experience.

Creating three independent systems drives up cost and complexity. Building a unified foundation and leveraging it across all three areas - is where real efficiency and scale emerge.

Compliance: From Periodic Audits to Continuous Monitoring

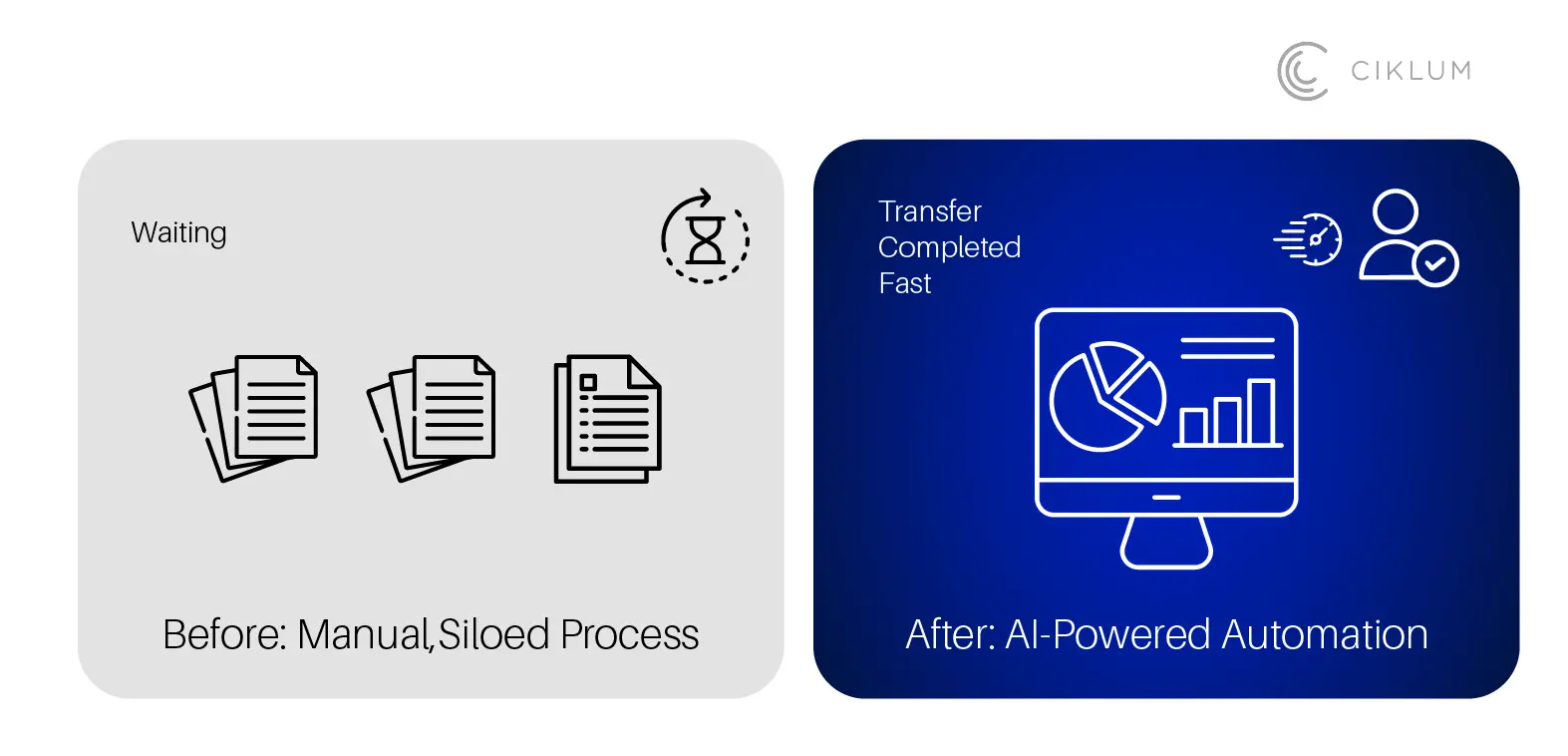

Compliance in financial services has traditionally been a periodic, manual exercise. Teams review transactions after the fact, pull samples, compare them against regulations, and produce reports. The process is labor-intensive, error-prone, and always behind.

AI automation changes the timing. Instead of reviewing samples of last quarter's transactions, systems can monitor every transaction in real time, flag anomalies, and generate audit-ready documentation continuously. BCG found that GenAI in banking compliance can improve KYC costs by 20% and boost file-closure rates by 67%. But fewer than 10% of banks have scaled these capabilities beyond pilot programs.

The core operational challenge is data. Compliance depends on extracting information from core banking systems, customer records, transaction logs, and regulatory databases - but when these sources remain siloed (as 57% of banking executives report), AI lacks the unified data it needs to generate meaningful insights.

Ciklum partnered with Santander Portugal to address a compliance-heavy operational challenge. The bank was handling more than 100 mortgage transfer requests per day through the Portuguese Banking Association, each requiring document processing, correspondence management, and signature validation within an 8-day regulatory SLA. Manual workflows proved slow and prone to errors. To solve this, Ciklum implemented an automated solution on Appian, combining RPA with intelligent document processing. The result was consistent SLA adherence, fewer document errors, and a significant release of FTE capacity - all delivered within 11 months.

In a broader context, agentic RAG systems are emerging as the architecture of choice for compliance automation. These systems retrieve relevant regulatory context in real time (GDPR, SOX, PSD2, AML directives), reason over it alongside transaction data, and produce outputs that include citations back to the source regulation. That traceability is what makes the output auditable, which is the non-negotiable requirement for any compliance automation in financial services.

Fraud: Speed and Accuracy at the Same Time

Fraud detection has been used for machine learning for years. What is changing is the integration of generative AI and agentic systems that can handle the unstructured, context-dependent aspects of fraud investigation that traditional ML models miss.

A rule-based system flags a transaction as suspicious. An ML model scores its probability of fraud. But the investigation that follows, reading the customer's history, checking related accounts, reviewing correspondence, pulling external data, has been manual. That investigation is where the bottleneck sits, and it is where generative AI fits.

Deepfake incidents in fintech increased 700% in 2023, making identity verification a fast-moving target. Traditional e-KYC processes that compare a selfie against an ID photo are being defeated by synthetic media. The response requires continuous adaptation rather than static rules, which is exactly what AI systems do better than manual review teams.

Ciklum's work in fraud prevention technology covers the full spectrum, from transaction monitoring and AML compliance to identity verification and audit trails. The pattern across deployments is consistent: AI handles the high-volume screening and initial investigation; humans handle the escalated cases that require judgment and regulatory accountability.

Customer Experience: Simplicity Over Feature Overload

The temptation in BFS customer experience is to add features:

A chatbot here, a dashboard there, a personalized notification. But the customer experience improvements that matter most in financial services come from removing friction in back-office processes, not from front-end additions.

When mortgage transfers move faster, customers receive their loans sooner. When fraud detection becomes more precise, legitimate transactions flow without disruption. When compliance reporting runs continuously, account openings no longer stall in manual KYC queues. Customers may never see automation - they simply experience smoother journeys, faster outcomes, and fewer issues along the way.

Ciklum helped Inspira Financial address exactly this. The financial services company, which combines health, wealth, retirement, and benefits offerings, was dealing with slow transaction processing and high error rates from complex integrations across banking partners. Ciklum deployed Salesforce as the core processing platform with MuleSoft as the integration hub, automating transaction flows both internally and externally. The impact: a 25% reduction in operational costs, 40% faster transaction processing, and a 30% improvement in data accuracy. With back-end friction eliminated, delays and errors decreased - leading to a measurable uplift in customer satisfaction.

The Shared Foundation

The most efficient approach treats compliance, fraud, and CX automation as layers on a shared data and integration foundation rather than as three independent projects. That foundation includes centralized data pipelines that connect core banking, CRM, transaction systems, and regulatory databases. It includes standardized integration (API-led connectivity, event-driven patterns) so that new capabilities can be added without rebuilding existing connections. And it includes governance: audit trails, role-based access, and human-in-the-loop controls for actions with regulatory consequences.

Our payment gateway solution for a multinational card services company shows what this foundation looks like at scale: 200+ API integrations across 16 EU countries, PSD2 compliance built into the architecture, 99.8% uptime, and a customer satisfaction score that increased from 2/10 to 9/10. This wasn’t the result of a standalone CX initiative - it was driven by reliability and compliance working together.

KPMG's 2025 banking survey found that financial services leaders rank data-driven personalization (91%), security and fraud prevention (89%), operational efficiency (88%), and regulatory compliance (88%) as their top investment priorities. Those numbers are nearly identical and that is the point. The underlying infrastructure required to deliver on each of them is the same.

Conclusion

Most financial institutions still view compliance, fraud, and customer experience as separate domains with separate budgets, teams, and technology stacks. That approach worked when each challenge was simpler and systems operated in isolation. Today, it no longer does.

The institutions that are gaining an edge are the ones that recognized the overlap early. The same data pipelines, integration layers, and governance frameworks can support all three. Build the foundation once, apply it across the organization, and the cost of adding new capabilities drops dramatically. Keep funding them separately, and you end up paying three times for infrastructure that should exist just once.

Technology itself isn’t an obstacle. The real challenge lies in the organizational shift-moving from treating these as three independent problems to building a single, unified foundation.

In short: treat the organization like one system, not three separate departments. Build the foundation once, and every new capability becomes faster, cheaper, and more effective.

By Ciklum Editorial Team

Ciklum’s Editorial Board is a collective of experienced writers and industry experts, bringing together perspectives shaped by real-world engineering and delivery experience. Through collaborative insights, the team explores how technology, AI, and digital innovation move from concept to execution across industries.

Blogs

Discover Similar Insights

Payments Without Friction: Modern Checkout Is Your Competitive Edge

Learn More

Modern Data Technology: Building an AI-Ready Data Infrastructure for Enhanced BFSI Analytics

Learn More

Agentic RAG in Banking: 5 AI Use Cases for Fraud Detection and Regulatory Compliance

Learn More

The Impact of GIS Data on the Insurance Industry: A Strategic Framework

Learn More