The next big wave in financial innovation is already rising, and Third-Party Providers (TPPs) are poised to ride its crest.

Back In 2016, when PSD2 flung open the doors to Open Banking, the digital payments landscape was reshaped by a handful of agile first-movers, who seized the moment and redefined it. Now, history is repeating itself as we stand at a similar inflection point. The arrival of PSD3 and the Financial Data Access Regulation (FIDA) is about to do for open finance what PSD2 did for payments. However, this time, the transformation will extend beyond payments into the full spectrum of open finance.

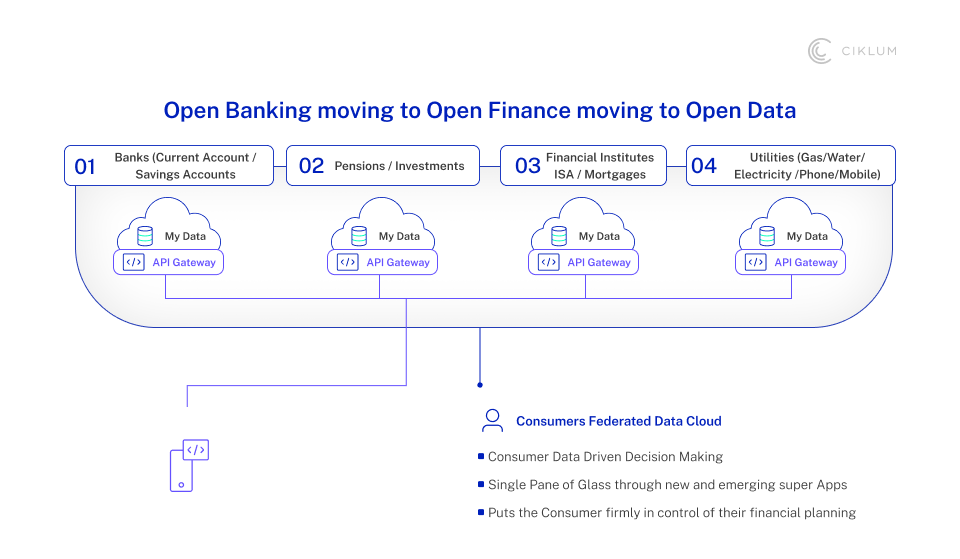

As the transformation increases its pace, soon, data from investments, savings, insurance, pensions, mortgages, utilities, and even public sector services will flow within a regulated, consent-driven framework. The winners will not just access this data – they’ll turn it into secure, personalized, real-time experiences. Experiences that will deliver tangible value for customers.

The next frontier won’t be defined by how many APIs a company connects. It is about who can turn chaotic, multi-source data into insight and impact – who can transform complexity into clarity, and that’s where AI becomes the ultimate differentiator.

The Change that is Coming

Think back to the early 2010s when PSD2 opened the door for TPPs to access bank account data. Those who moved fast gained massive advantage. Now, a new chapter is unfolding. PSD3 and FIDA mark the next major leap, one that expands beyond payments into the broader world of open finance. Soon, all the data from savings, insurance, investments, pensions, mortgages, utilities, and even government-held financial data will be accessible through consent-based sharing.

The "PSD2 moment" is again setting the stage in the broader market. The first-movers gained rapid growth, loyal user bases, and data-driven business models back in 2016 – something the most forward thinking providers can never forget. But this time, the playing field is wider. With FIDA’s sweeping scope, open finance will touch every corner of a customer’s financial data, creating the foundation for a seamlessly connected ecosystem.

For TPPs, this evolution means they must shift from accessing bank data to orchestrating complete, multi-dimensional financial experiences. As the regulatory framework shifts from open banking to open finance, it will reshape how financial data is created, shared, and monetized.

Why This is a Challenge for TPPs

The opportunity ahead is huge, but so is the complexity. For third party providers, shifting from open banking to open finance means dealing with new data types, new standards, and new dependencies.

1. Inconsistent data

TPPs must gather and standardize information from many different sources. There is a matter of caution however, since TPPs depend on aggregating and harmonizing data from banks, insurers, pension administrators, investment firms and beyond. Each source operated with its own data formats, refresh rates, and integration quality. Here, delivering a unified customer experience becomes challenging as the result is often a patchwork of inconsistent data.

2. Data quality and timelines

Even when data is available, it might be incomplete or outdated. A provider might receive a customer’s savings balance data but miss their latest pension contributions or investment updates. Open finance heavily relies on high-quality, real-time data, and when either falls short, customer confidence quickly erodes.

3. Reliance on external partners

Aggregation in real work depends on multiple upstream providers. While one bank may have a well-functioning API, another’s might lag behind or expose only limited data sets. This dependence creates friction, delays, operational latency, and risk that are largely beyond the TPP’s direct control.

If we sum this up into one statement: data access alone is not enough. To succeed and thrive in open finance, TPPs must go beyond connectivity and deliver data that is accurate, complete, and harmonized. This is the foundation of every intelligent, value-added service. Without this, they risk being seen as intermediaries, not as innovators.

How AI and Ciklum’s AI Incubator Can Help

Artificial Intelligence is now an essential toolkit for TPPs to overcome these barriers – turning fragmented, inconsistent data into value that drives growth. As the era of open finance flows, the AI engine can power smarter decisions, faster innovation, and stronger customer engagement.

1. Faster ideation, validation, and testing

In a market evolving as fast as this one, speed matters. TPPs need a way to move from concept to validated solution in weeks – not in months. With Ciklum’s AI Incubator, organizations get a pathway to ideate, validate, and test AI use cases at enterprise speed. By combining rapid prototyping, customer validation, and built-in firebreaks, TPPs can identify potential by testing, learning, and scaling only the ideas that prove real business value.

2. Hyper-personalization powered by smarter data

With FIDA unlocking broader data access, TPPs can personalize services like never before. AI models can now connect information across savings, investment, insurance and pension data to predict needs, detect life events, and trigger timely recommendations. For example, when a pension contribution stops, AI could identify and prompt an engagement campaign and propose a tailored savings or investment plan. This level of proactive service builds loyalty and trust, while turning potential churn into renewed engagement.

3. Data harmonization and quality assurance

One of AI’s biggest advantages is its ability to clean, enrich, and standardize data across multiple sources. Using techniques such as anomaly detection, intelligent data mapping, and missing-value prediction can help TPPs transform disjointed inputs into reliable insights. Ciklum’s AI Incubator provides ready-to-use frameworks and pre-built accelerators that make this practical. Ciklum’s advanced models can track API performance, monitor uptime, flag latency spikes, or rate data freshness in real time. This gives TPPs the confidence that every decision is powered by consistent and accurate data.

4. Laying the groundwork for open finance

Prototyping and validation aren’t the finish line – they’re the foundation for scalable success. With Ciklum’s AI Incubator’s 6–10 week model, TPPs to create feature-ready prototypes that evolve into production-grade solutions with accuracy. And once FIDA takes effect, these validated prototypes become the architectural backbone for broader financial data integration. Getting started ahead of time means being ready to lead when regulations take effect, instead of scrambling and then burning resources to catch up.

5. Delivering measurable outcomes, not demos

Many innovation programs stop at proof-of-concept. The AI incubator prioritizes tested, validated prototypes that deliver clear ROI instead of just focusing on proof-of-concepts. This means TPPs can easily shift from experimentation to execution with confidence – faster. The result is a working product, not just a demo - AI-driven, data-rich, ready to personalize experiences, automate decisions, and deliver tangible business value.

What TPPs should do now

To prepare for the open finance era, TPPs should begin taking structured action today.

- Map the opportunity: Identify which new data types – savings, pensions, insurance, mortgages - are relevant to your customers.

- Assess data quality: Audit your current data stack for consistency, latency, and completeness.

- Select impactful use cases: Focus on AI-driven initiatives that generate measurable business outcomes, such as churn reduction or personalized investment recommendations.

- Prototype through validation frameworks: Use an incubation model to test, refine, and validate ideas in weeks instead of months.

- Strengthen data governance: FIDA will require robust consent management, transparency, and auditability. Build these controls early.

- Plan for scalability: Ensure your AI and data infrastructure can handle multi-domain integration and real-time data updates.

By following these steps, TPPs can position themselves to move first, validate faster, and capture market share as regulation evolves.

The Road Ahead for TPPs

The shift from open banking to open finance marks one of the most significant turning points in the European financial ecosystem. The PSD3 and FIDA frameworks are not just regulatory milestones – they are catalysts for a smarter, more connected financial ecosystem, and gateways to a new era of customer experience.

The path lies forward for TPPs. Success in this landscape depends on turning data complexity into actionable intelligence. The key enabler is AI, that provides the capability to unify fragmented data, predict customer needs, and deliver hyper-personalized financial journeys.

This is where Ciklum’s AI Incubator delivers impact. Ciklum’s AI Incubator combines rapid ideation, validation, and feature-ready prototyping, empowering organizations to test real-world AI use cases and scale their AI-driven solutions rapidly.

The formula for leadership in open finance is simple: Validate earlier. Build faster. Scale smarter. The Open Finance era belongs to those who act now and start building it today.

By Mark Westbrook

Global Head of Architecture

18+ Exp

Mark brings 18+ years of payments expertise, spanning POS, Open Banking, and Core Payment Rails. As Global Solutioning Director, he crafts innovative strategies that drive operational excellence across payments and banking.

Blogs

Discover Similar Insights

The Agentic Shift: Rewiring the Retail Operating Model

Learn More

Agentic AI in Retail: Closing the Gap Between Customer Intent and Enterprise Systems

Learn More

From AI Interest to Engineering-Ready Mandates: Why The Market Needs AI Clinics, Not More AI Pilots

Learn More

Agentification of Payments: A Strategic Shift for PSPs

Learn More