Key Takeaways:

- Regulators now require banks to explain AI-driven decisions, making "black box" models a compliance liability

- Explainable AI builds customer trust by providing clear reasons for credit decisions

- Modern interpretable models can achieve competitive accuracy while maintaining transparency

- A phased approach to XAI adoption reduces risk while building organizational capability

Introduction: The Transparency Imperative

Artificial intelligence is transforming how banks assess credit risk, detect fraud, and manage compliance. From automated loan underwriting to real-time transaction monitoring, AI models now influence decisions that affect millions of customers daily.

But this transformation has created a challenge: many of these models operate as "black boxes." They produce accurate predictions, but no one can explain why a particular decision was made. When a customer asks "Why was my loan denied?" or a regulator asks "How does your model avoid discrimination?", banks using opaque AI systems often struggle to provide satisfactory answers.

This opacity is becoming untenable. Regulators worldwide are tightening requirements for algorithmic transparency. Customers expect clear explanations for decisions that affect their financial lives. And banks themselves need to understand their models to manage risk effectively.

Explainable AI (XAI) addresses this challenge by making AI decision-making transparent and auditable. For banking leaders, understanding XAI is no longer optional. It's essential for compliance, customer trust, and sound risk management.

Why Explainability Matters In Banking

As artificial intelligence reshapes the financial industry, the ability to understand, trust, and justify automated decisions has never been more important. Unlike traditional models, many advanced AI systems operate with a level of complexity that can obscure their inner workings, creating significant risks for banks, their customers, and regulators alike.

Transparent and auditable AI not only enables compliance, but also builds customer trust, supports ethical decision-making, and strengthens operational resilience in an increasingly data-driven world.

Regulatory Compliance

The regulatory environment has fundamentally shifted. Financial institutions can no longer justify deploying opaque AI systems on the basis of marginal accuracy improvements.

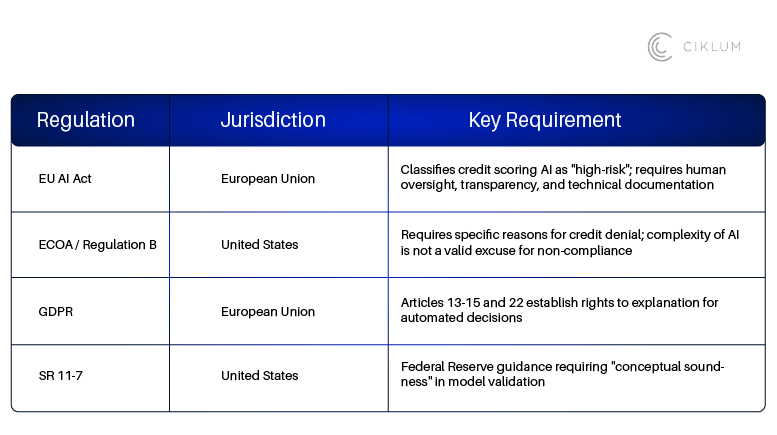

In the European Union, the EU AI Act explicitly classifies AI systems for credit scoring as "high-risk," triggering stringent requirements for transparency, human oversight, and technical documentation.

In the United States, the Consumer Financial Protection Bureau (CFPB) has clarified that creditors using complex algorithms cannot sidestep adverse action notice requirements by claiming their models are too complicated to explain. As stated in CFPB Circular 2022-03: "A creditor's lack of understanding of its own methods is therefore not a cognizable defense against liability."

The message is clear: if you can't explain your model, you may not be permitted to use it.

Customer Trust and Fair Lending

When customers understand the reasons for credit decisions, they are more likely to accept outcomes (even unfavorable ones) if the logic is transparent and defensible.

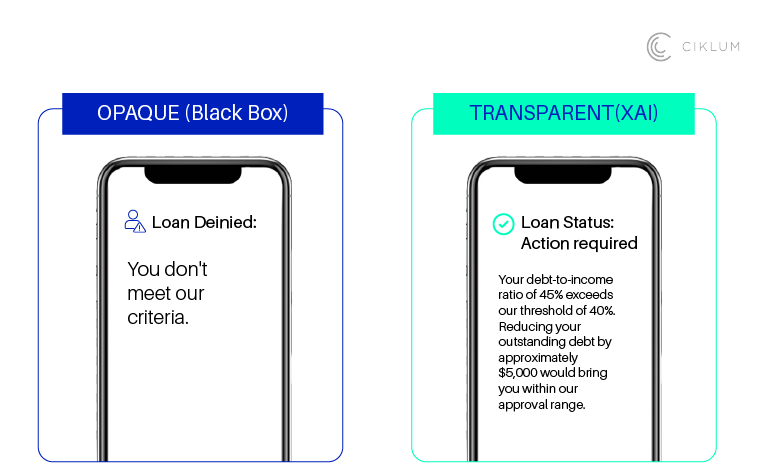

Consider two denial scenarios:

- Opaque: "You don't meet our criteria."

- Transparent: "Your debt-to-income ratio of 45% exceeds our threshold of 40%. Reducing your outstanding debt by approximately $5,000 would bring you within our approval range."

The second response builds trust, provides actionable guidance, and demonstrates fair treatment. It also creates a record that can withstand regulatory scrutiny.

Bias Detection and Mitigation

Explainability is the primary tool for detecting algorithmic bias. When a bank cannot explain why approval rates differ by demographic group, it cannot diagnose and remediate the problem.

Interpretable models expose which features, or proxies for protected characteristics drive disparate outcomes. This visibility enables targeted interventions, such as removing employment gaps as a feature if it unfairly penalizes individuals with caregiving responsibilities.

For organizations committed to Responsible AI practices, explainability is foundational to ensuring fair treatment across all customer segments.

Operational Resilience

Explainable models are inherently easier to validate, monitor, and maintain. When model risk managers understand how a model works, they can:

- Identify when performance begins to degrade

- Diagnose root causes of unexpected behavior

- Implement remedial actions faster than with black-box systems

- Satisfy regulatory examination requirements

This operational resilience is increasingly valued by regulators, who have indicated that banks using more interpretable models may face less intensive supervisory scrutiny.

The Regulatory Landscape

The global trend is clear: transparency is becoming a prerequisite for AI deployment in banking. Organizations that invest in explainability now will be better positioned as requirements continue to tighten.

Technical Approaches to Explainable AI

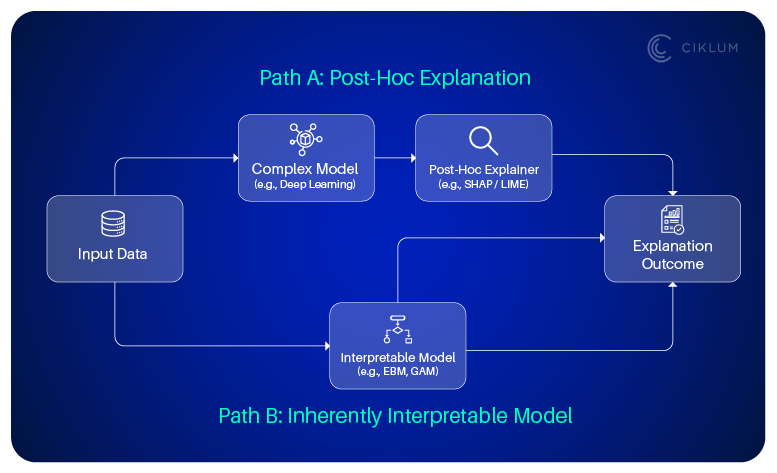

Banks can achieve explainability through two primary approaches: post-hoc explanation methods applied to complex models, and inherently interpretable model architectures.

Post-Hoc Explainability

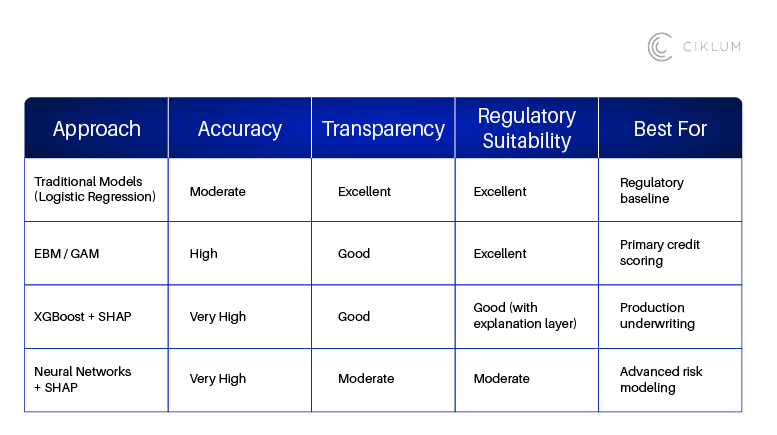

SHAP (SHapley Additive exPlanations) has become the industry standard for explaining complex models. Based on game theory, SHAP calculates the contribution of each input feature to a specific prediction. For credit decisions, this enables banks to identify which factors most influenced a denial and generate compliant adverse action notices.

SHAP provides both local explanations (why this customer was rejected) and global explanations (which features matter most overall), supporting both customer communication and model validation.

LIME (Local Interpretable Model-agnostic Explanations) offers a faster alternative by approximating complex models locally with simpler linear models. While useful for real-time explanations, LIME's results can vary between runs, making it less suitable for regulatory documentation where consistency is paramount.

Inherently Interpretable Models

Explainable Boosting Machines (EBMs) represent a significant advancement in interpretable modeling. EBMs combine the accuracy of gradient boosting with the transparency of additive models. Each feature's contribution can be visualized independently, allowing risk officers to inspect how the model treats variables like income or credit utilization across their entire range.

Neural Additive Models (NAMs) extend this approach using neural networks that attend to individual features independently. This preserves the non-linear modeling capability while maintaining the additive structure required for clear reason codes.

Choosing the Right Approach

The choice depends on the specific use case, regulatory requirements, and organizational capability. Many institutions deploy a combination: inherently interpretable models for core underwriting decisions, with post-hoc explainability for monitoring and validation.

Implementation Considerations

Start with High-Risk Use Cases

Prioritize explainability for decisions with the greatest regulatory exposure and customer impact: credit scoring, loan underwriting, and fraud detection. These areas face the most scrutiny and offer the clearest compliance benefits.

Integrate with Existing Governance

XAI should be embedded within your Model Risk Management framework, not treated as a separate initiative. Model validation procedures should assess explanation stability, fidelity, and consistency alongside traditional performance metrics.

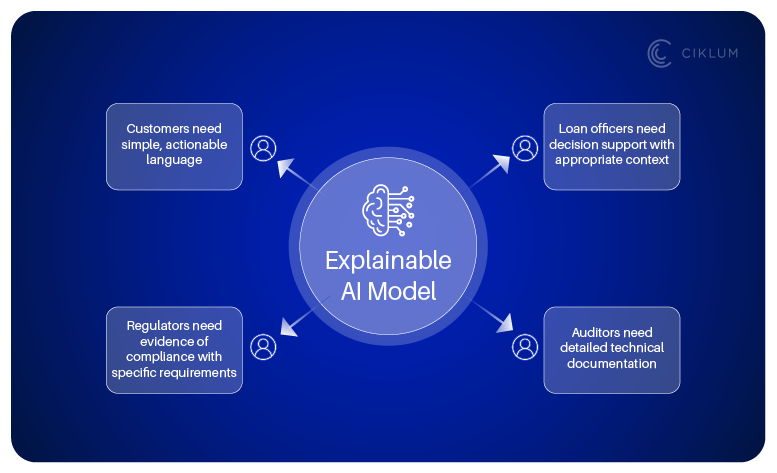

Design for Multiple Audiences

Effective explanations serve different stakeholders:

- Customers need simple, actionable language

- Loan officers need decision support with appropriate context

- Auditors need detailed technical documentation

- Regulators need evidence of compliance with specific requirements

Build systems that generate appropriate explanations for each audience from the same underlying model.

Plan for Continuous Monitoring

Explanations should be monitored over time. Alerts should trigger when feature importance rankings shift significantly, potentially indicating model drift or data distribution changes. This continuous validation ensures that explanations remain accurate as conditions evolve.

For organizations building AI capabilities, our AI Strategy, Enablement & CoE services can help establish governance frameworks that incorporate explainability requirements from the start.

Frequently Asked Questions

Not necessarily. Post-hoc methods like SHAP add transparency to complex models without changing their accuracy. Interpretable models like EBMs often match black-box performance on tabular financial data. Choose the approach that fits your use case and regulatory needs.

A single-system pilot (e.g., credit scoring) often takes 2–4 months. Broader deployment across systems and into Model Risk Management can take 6–12 months. Many banks start with one critical system, then scale.

Try post-hoc methods (SHAP or LIME) first. If needed, retrain with interpretable architectures like EBMs or GAMs. Regulators do not accept "we don't understand our model" as a defense; with the right approach, most models can be made sufficiently transparent.

By Aaron Jones

Global Head of Product & Experience

Aaron Jones is the Global Head of Product & Experience at Ciklum, where he drives the strategic vision for transitioning ambitious concepts into market-defining products that deliver measurable business impact. He also directs the global Experience Service Line, leading a team of several hundred product and experience practitioners worldwide.

Blogs

Discover Similar Insights

Agentic AI in Retail: Closing the Gap Between Customer Intent and Enterprise Systems

Learn More

From AI Interest to Engineering-Ready Mandates: Why The Market Needs AI Clinics, Not More AI Pilots

Learn More

Agentification of Payments: A Strategic Shift for PSPs

Learn More

Payments Without Friction: Modern Checkout Is Your Competitive Edge

Learn More