Key Takeaways:

- Customer expectations for fast, frictionless payments are rising sharply

- Maximum choice, including digital wallets and Open Banking, is essential

- Smart technologies, fully integrated, can help businesses maximize revenue opportunities

- Expert tech support is vital to turn concept into successful reality

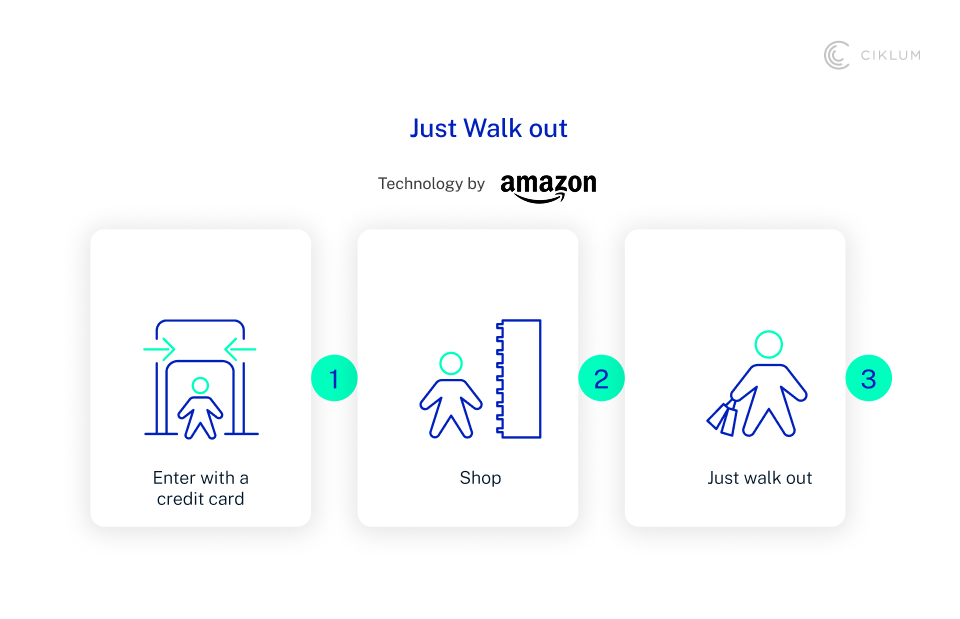

As the world of retail continues to evolve, modern technology has a vital role to play in helping customers pay as easily and quickly as possible. And this applies just as much at checkouts in physical stores as it does when buying goods and services online. Amazon’s cashless stores, based on “just walk out” technology, are an excellent example of how technology can completely transform even the most everyday shopping experiences.

However, many organizations still rely on outdated payment systems that struggle to keep up with these rising expectations. As Payment volumes surge and methods diversify - driven by mobile wallets, Open Banking, and real-time instant settlements, legacy technologies reveal critical limitations.. These systems often lack modern API readiness, making real-time integration with partners and fintech ecosystems difficult. Manual reconciliation processes slow down operations, introduce risk, and delay customer-facing updates. The world of payments is seeing an indisputable rise of real-time transactions in major markets like the UK, Europe and the US, making it critical for underlying payment infrastructure to keep pace.

In this rapidly evolving landscape, the question remains: are your payment systems helping you delight customers – or costing you their business? With the future of cashless payments evolving so quickly, the following sections explore common payment challenges and how new technologies are addressing them in practice.

Challenges Associated with Common Payments Technologies

Making payment and checkout experiences seamless and user-friendly can often prove easier said than done. From traditional self-checkout to advanced RFID-enabled cashless payments, many retailers and financial institutions have faced practical challenges integrating the technologies they want to use, while still meeting the rising expectations of consumers. These challenges include (but are not limited to):

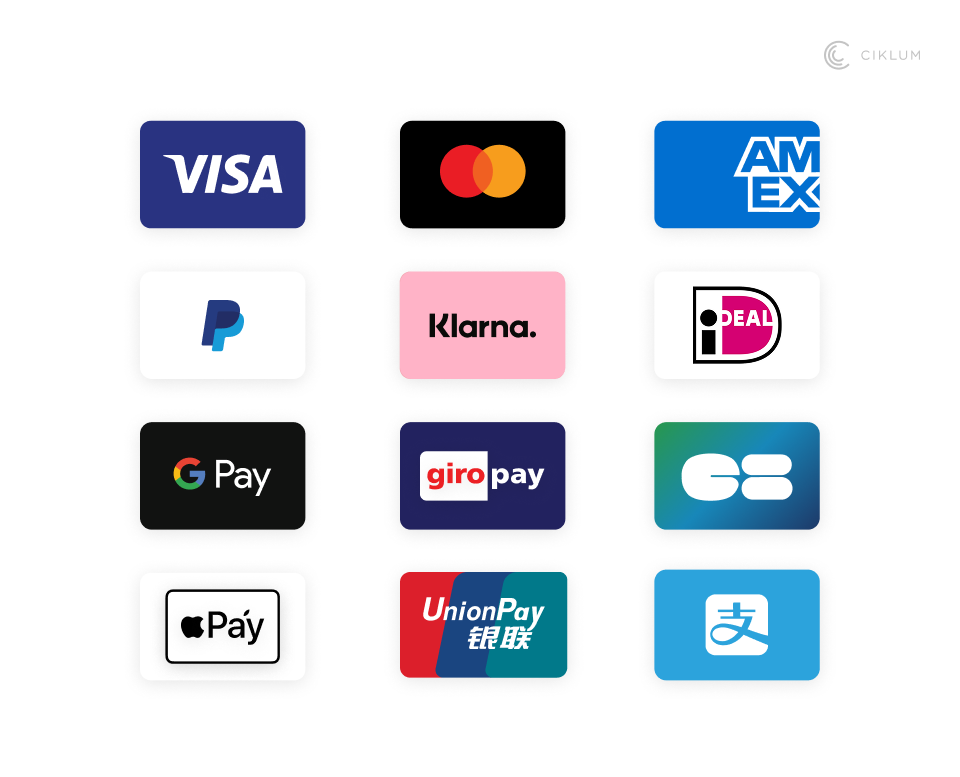

Limited Payment Options

Nearly 13% of online shoppers abandon their carts because the store didn’t offer a payment method they preferred. It’s clear that customers want the maximum choice available, so they can always pick the payment option they’re familiar with – whether that’s a traditional card, an Open Banking transfer, an alternative method like PayPal, or a Buy Now Pay Later (BNPL) plan. Failing to provide a favored payment option means losing out on conversions.

Outdated Technology

Customers increasingly expect to pay without having to manually key in any card details, thanks to mobile wallet technology such as Apple Pay and Google Pay. They are likely to favor businesses that support these conveniences over those that don’t. The gap is often due to outdated back-end systems. Many core payment platforms in use today were not designed for a 24/7 real-time processing environment, resulting in clunky workflows and even manual steps for certain transactions.

In fact, 70% of banking leaders surveyed admitted they are not confident in their existing payment infrastructure’s readiness to provide modern services. Legacy payment systems that require manual checks or batch processing lead to inefficiencies and slow service, raising operational risks – and frustrating tech-savvy customers who expect instant, hassle-free payments.

Lack of Personalization

Research has found that retailers can boost sales by up to 20% by personalizing the checkout experience – for example, applying loyalty rewards or tailored offers based on a customer’s shopping history. Shoppers have come to expect payment experiences (and available options) to be similar across in-store and online channels, so they can pay with confidence and not end up surprised or frustrated by the process. But when payments feel disconnected - like failing to recognize a returning customer or not surfacing relevant offers -it erodes confidence and leads to frustration.

One clear opportunity lies in intelligent automation at checkout. For instance, auto-applying loyalty points or suggesting a preferred payment method based on past behavior. These small, personalized touches not only remove friction but also reinforce customer trust and drive repeat business. Retailers and BFSI providers that fail to deliver these experiences risk missing critical moments to convert and retain valuable users.

Limited Global Support

Customers want to be able to buy from anywhere in the world without worrying about currency or payment method restrictions. Developments such as the European Union’s Single Euro Payments Area (SEPA) are designed to facilitate easy cross-border transactions in Europe; retailers or payment providers that don’t support multi-currency and international payment options will lose out on global customers. As ecommerce becomes increasingly borderless, outdated systems that can’t handle foreign currencies, local payment methods, or new cross-border payment rails will be a barrier to growth.

Smart Technologies Addressing Payments Challenges

None of the above challenges are insurmountable. In fact, many forward-thinking retailers and banks have been adopting technologies that automate, streamline, or secure payment flows– and modernizing their legacy platforms – as a way of overcoming these issues and reaching customers like never before. Modern, integrated payment solutions provide the scalability, automation, and security needed to manage today’s complex mix of payment methods.

Through 2025 and beyond, the payments landscape is being reshaped by numerous innovations, including biometric authentication, voice-activated commerce, mobile cashless payments, account-to-account (A2A) transfers, real-time payment networks, and various other forms of cashless transactions. However, a few particular technologies stand out as driving some of the most significant changes:

Digital Wallets, ‘Super Apps’, and Click to Pay

Digital wallets are set to dominate online payments, with over 50% of global eCommerce transactions expected to be wallet-based by 2026. Super apps like PayPal, WeChat Pay, and Alipay already combine payments, banking, and loyalty into a single experience - but convenience is now being redefined at checkout.

That shift is being driven by Click to Pay, an emerging industry standard that enables frictionless, card-based checkout across browsers. Powered by FIDO authentication and passkeys, Click to Pay removes the need for passwords or manual card entry. Instead, users authenticate securely using biometrics such as fingerprint or facial recognition, supported natively by browsers like Chrome, Safari, and Firefox.

By reducing friction and improving security, Click to Pay helps lower cart abandonment while setting a new baseline for fast, seamless digital payments.

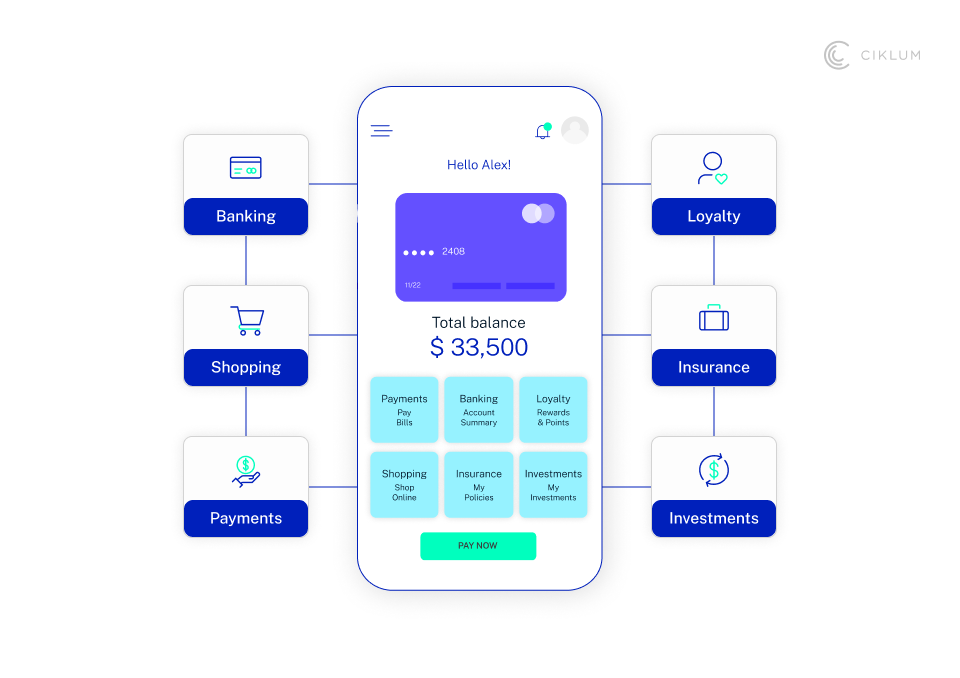

These all-in-one apps enable customers to handle virtually all their financial dealings more easily than ever – from everyday purchases to investments – within a single ecosystem. Retail technology development is moving quickly in this direction. Ciklum is already working with one client on a fully integrated “super app” approach, combining multiple financial services and payment capabilities into a seamless user experience. Businesses that tap into the super-app and digital wallet trend can stay closer to their customers’ daily financial lives, whereas those that stick to outdated payment interfaces may find themselves sidelined.

Open Banking Payments

Open Banking payments (bank-to-bank digital payments initiated via secure APIs) are relatively low-cost for merchants to process, which means they represent a huge opportunity to offer payment flexibility while protecting profitability. In addition, they remove dependence on card networks for certain transactions. This is especially the case in regions like the United States, where Open Banking is quickly gaining tractionciklum.com.

In markets such as the UK where Open Banking was introduced earlier, adoption has accelerated dramatically – 13.3 million consumers and small businesses were active open banking users in the UK as of early 2025, a 40% increase from the year before. In fact, over 31 million Open Banking payments were made in the UK in a single month (March 2025), accounting for nearly 8% of all electronic payments that month. This surge illustrates the enormous appetite for account-to-account payment options. It also underscores why Open Banking is a focus for banks and fintechs worldwide, not just in Europe – the momentum is spreading globally as regulators and tech providers enable similar frameworks elsewhere.

From Transactions to Trust: How Data Personalization Drives Loyalty

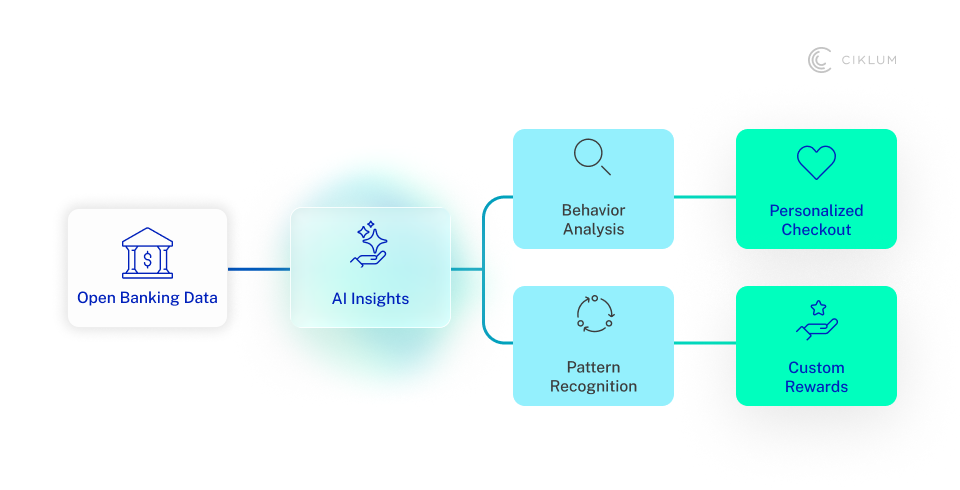

One way to maximize the potential of Open Banking is to leverage the rich data it provides (with customer consent), such as transaction histories and spending behavior. This data is key to personalizing payment experiences and loyalty rewards for each individual customer, meeting their expectations in real time.

It’s why we at Ciklum are focusing on unlocking this opportunity for retailers and businesses around the world. Open Banking capabilities should form part of a wider personalization strategy that also integrates artificial intelligence and machine learning to tailor the buying journey from start to finish. For example, beauty retailer Sephora has excelled at this by leveraging user-generated data (like customers’ uploaded images and past purchases) to provide personalized product suggestions; these insights even arm in-store advisors with real-time recommendations for shoppers. Similarly, banks can use Open Banking data combined with AI to offer personalized financial advice or custom-fit products, enhancing customer loyalty.

Explore Ciklum’s Smart Payments Technologies

To make the most of all the opportunities that smart payments can deliver, it’s important to work with an expert technology partner that can support you from initial concept through development to successful implementation. Ciklum brings proven experience in modernizing legacy infrastructure, increasing checkout conversion rates, reducing fraud risk, and enabling scalable, personalized payment ecosystems across global markets.

Examples of our success in the BFSI and payments sector include:

- Future-proofing payment infrastructure for Swedish gaming company Betsson – delivering a modern payment platform that covers multiple jurisdictions and enabling millions of transactions to be processed every day.

- Developing a mobile app for a UK-based FinTech business, empowering business owners to understand their sales activity through AI-generated insights (bringing advanced analytics to their fingertips).

- Partnering with Stripe’s payment technology experts to empower customers with hyper-personalized payment experiences – from optimized online checkout conversions to smooth mobile payments integration.

We can deliver the same level of innovation and integration for your in-store, online, and back-end payment experiences as well. Get in touch with our team today to find out more about transforming your payment systems and delighting your customers.

By Aaron Jones

Global Head of Product & Experience

Aaron Jones is the Global Head of Product & Experience at Ciklum, where he drives the strategic vision for transitioning ambitious concepts into market-defining products that deliver measurable business impact. He also directs the global Experience Service Line, leading a team of several hundred product and experience practitioners worldwide.

Blogs

Discover Similar Insights

From AI Interest to Engineering-Ready Mandates: Why The Market Needs AI Clinics, Not More AI Pilots

Learn More

Agentification of Payments: A Strategic Shift for PSPs

Learn More

Explainable AI in Banking: Designing Transparent, Auditable Models for Credit, Risk, and Compliance

Learn More

Enterprise AI Automation: A Practical Guide to GenAI, AI Agents and Intelligent Workflows

Learn More