It’s been six years since Open Banking (OB) arrived in the UK, but the jury is still out as to the scale of its potential, and its success so far. Imran Gulamhuseinwala, Ciklum’s Open Banking Advisor, explored this mixed narrative at a recent event on payments innovation hosted by FSTech, drawing on his experience leading the UK’s initiative on OB.

Since 2018, when British banking giants were first required to set up APIs that enabled customers to share current account data with third-party FinTech firms, a raft of new innovations and finance businesses have entered the marketplace. Despite OB allowing individuals to take control of their data and payments, uptake has been limited so far. According to Imran, there are currently around seven million active OB users in the UK, which is well short of expectations. So where has OB seen success, what are the challenges to wider adoption, and what does the future hold? Imran explained it as a story of two halves: “Just as many people will say that Open Banking has been a success than say it’s been a failure,” he said.

“On the one hand, we’ve got excellent coverage in the country: something like 95%+ of all banks have really high quality APIs that are standing up and working well. And we've got 300+ participants in the Open Banking ecosystem. But on the other hand, penetration is around about 11%, so only one in nine digitally active consumers are using it. When you look at the demand side, still the public have very low familiarity with Open Banking: they have a low understanding of what it actually is and trust is also very low as well.”

Open Banking’s success story so far

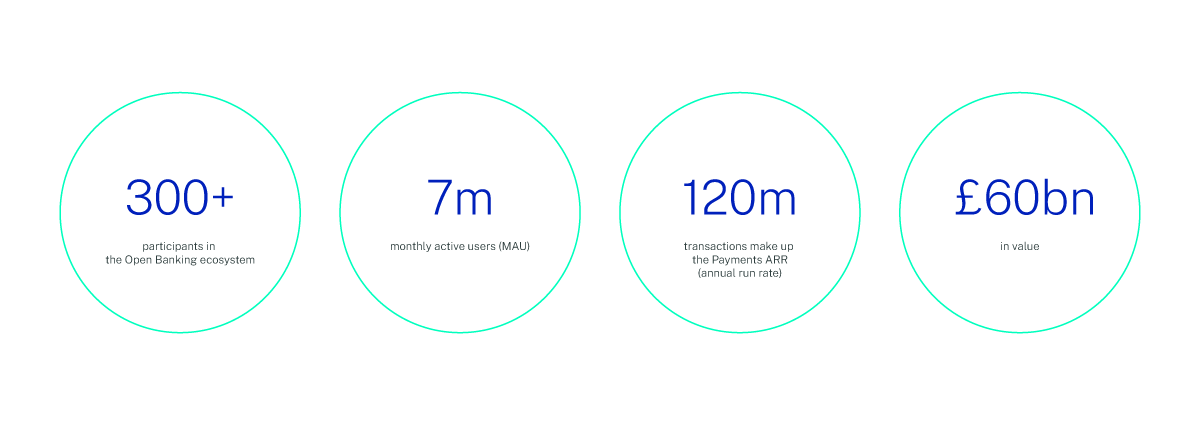

Imran was keen to underline some of the headline figures around the headway that OB is making in the UK: “We've got 300+ participants in the Open Banking ecosystem. Seven million customers are using it, and that's monthly active users (MAU). Payments ARR (annual run rate) is running at about 120 million transactions. And in terms of value, we're around £60 billion.”

From a retail perspective, the deprecation of third-party cookies has resulted in many market leaders turning to OB in order to maintain the success of their loyalty programs. As they can no longer rely on cookies for demographic information, they need first-party data instead.

“You're seeing a lot of smaller retailers even here in the UK bombarding you with ‘join my loyalty program, join my loyalty program, join my loyalty program’” Imran explained. “This is what's underpinning some of that. And then I think on top of that we've also got retailers beginning to understand the benefits of non-card payments, and the benefits of closed-loop networks.”

Similar successes have been found in the movement of point-of-sale (POS) terminals to the cloud and using gift cards for cashback, both of which are growing trends in the OB space. “[POS terminals] used to be very much static bits of kit, and now they’re very much more cloud-based and, as I understand it, Android operating systems are becoming de rigueur across many of them.”

Challenges along the way

While penetration rates for OB rise from 11% overall to 17% among small and medium enterprises (SMEs), around half of the uptake is attributed to HMRC and the facility to use OB for self-assessment tax returns.

Imran expressed a view that much of this low take-up was down to trust, and a wariness among the public around moving away from the traditional banking infrastructure they have relied upon for decades. “When it comes to consumer behavior, force of habit, familiarity, and trust are a virtuous circle. The more people use it, the more they'll trust it. People have trusted banks for decades and it’s a system they know not only works, but it’s something they trust and feel secure about. Pitching Open Banking and its benefits to them is harder than one might think.”

At the same time, many OB providers are still struggling to achieve profitability, or to reach the level of investment returns that their venture capital backers were expecting or hoping for. Much of this may be down to traditional banks’ reluctance to support OB, something that may be eased by allowing banks to charge for ‘premium’ APIs.

Security also remains a major and sensitive issue in Open Banking, for two reasons. The first comes down to decision-making. As technologies converge and evolve, the question arises: who wields the authority over decision-making? Is it the Chief Information Security Officer (CISO), given the impact of security concerns on IT infrastructure? Or perhaps the Chief Marketing Officer (CMO), tasked with spearheading growth initiatives? These conflicting internal agendas could introduce vulnerabilities into security protocols. The second relates to fraud mitigation efforts, where many cybercriminals hold the edge on FinTechs in terms of security resources and expertise. Given that third-party providers are often emerging FinTechs with limited experience in combating financial crimes, malicious actors can masquerade as these providers, complicating the distinction between fraudulent activities and genuine transactions.

What does the future hold for Open Banking?

Despite the challenges, Imran sees great opportunity for OB, by bringing payments, loyalty and data together: “We are already beginning to see what I describe as experimentation in the Open Banking data to power loyalty space. Players like Nectar and Cardlytics are doing a decent job… of looking at how this works.” There are two principal drivers behind this: consumers being more receptive to a loyalty proposition than one from a financial services company, and that loyalty schemes are able to offer much bigger incentives to customers than are possible in other areas.

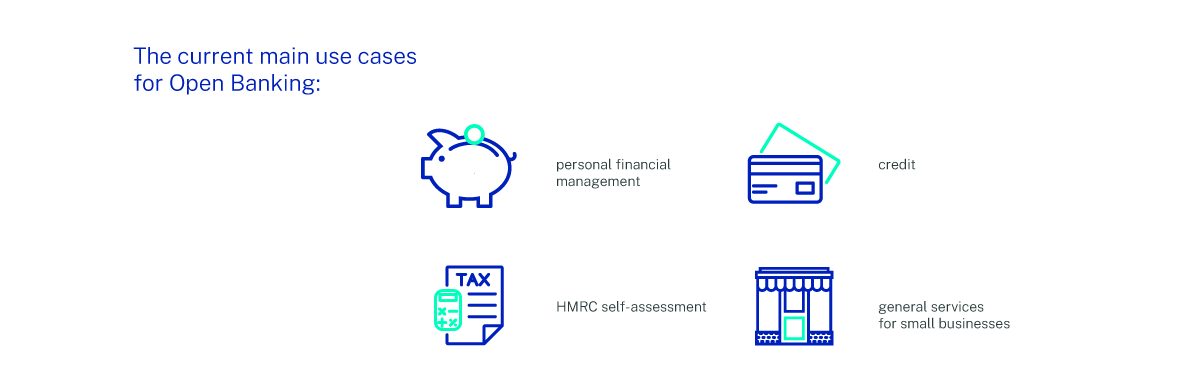

The current main use cases for OB are around personal financial management, credit, HMRC self-assessment, and general services for small businesses. While these are all sizable in market terms, they remain relatively niche in nature. What Imran foresees is a further expansion of use cases in the months and years ahead, into areas full of potential that have remained untouched or relatively unexplored up to this point.

Alongside variable recurring payments (VRP) for eCommerce and consumer protection, Imran singled out Open Finance as a potential growth area, especially in the UK: “Open Finance, that really was the promise behind Open Banking. So the consumer could see all of their financial relationships in one place, not just the current accounts, which is what Open Banking is. And when you look at other countries, they don't even consider Open Banking. They consider Open Finance. They're looking to leapfrog that immediately.”

Looking further ahead, the introduction of CBDCs and cryptocurrencies more widely will, in Imran’s view, pose further challenges around consumer education and building trust. If it’s too difficult to use and to adopt, then people simply won't do it due to the added friction - they'll revert back. Although we may be far off from seeing OB widely adopted, there is potential for it to really benefit the system.

Can Open Banking become a mainstream payment rail?

Imran was also keen to explore the monetization and sustainability of OB going forward, but doesn’t believe that it is suitable as a payment rail in itself, at least in the short term.

“[Open Banking payments are] not a payments rail. It's purely an instruction layer that initiates payments which are then passed to the rail,” he said. “So, pretty obviously, Open Banking payments can only be as good as the underlying payment rail. And we have a problem in this country - faster payments. It's simply too expensive. It's a good product, but it is expensive. And when you factor in that the provider has to include a margin on top of the cost of faster payments, you find that it doesn't compete that well with debit cards.”

Imran was also skeptical about VRP as an area for growth in OB providers, for much the same reason: “I think also another problem is that the VRPs are being pushed more towards a replacement for direct debits. I can see that as being a really good user experience because VRPs give the consumer much more control than direct debits do, which tend to be open-ended and hard to manage. But it's really hard to see direct debits being displaced from an economic point of view because they are very good at what they do, they're very cheap.”

However, on a more positive note, Imran encouraged the attendees to keep an eye on the iGaming and online gambling sector - especially in the United States - as a key driver of OB innovation: “A lot of cards bounce because in some states gambling is illegal and the cards try and geolocate it and get themselves in an awful muddle, which has left the door open for Open Banking providers. Also, payout is a massive part of closing the loop, which you can get there quicker through account-to-account payments, particularly now with FedNow.”

In summary

Overall, despite the headwinds that are beginning to be addressed, Imran painted an optimistic picture for Open Banking’s future. It has a chance to become a genuine challenger to the traditional card monopolies, and is helping revolutionize point-of-sale and eCommerce journeys, especially through the integration of loyalty programs and payments.

Want to drive new Open Banking solutions? Need help with your underlying technology stack? Get in touch with Ciklum’s expert team today and let’s discuss your specific use cases and requirements.

By Ciklum Editorial Team

Ciklum’s Editorial Board is a collective of experienced writers and industry experts, bringing together perspectives shaped by real-world engineering and delivery experience. Through collaborative insights, the team explores how technology, AI, and digital innovation move from concept to execution across industries.

Blogs

Discover Similar Insights

The AI Readiness Gap: 5 Blockers Causing Most AI Failures

Learn More

AI Automation in BFS: Strengthening Compliance, Fraud Prevention, and CX

Learn More

Payments Without Friction: Modern Checkout Is Your Competitive Edge

Learn More

How to Choose a Software Development Company in 2025

Learn More