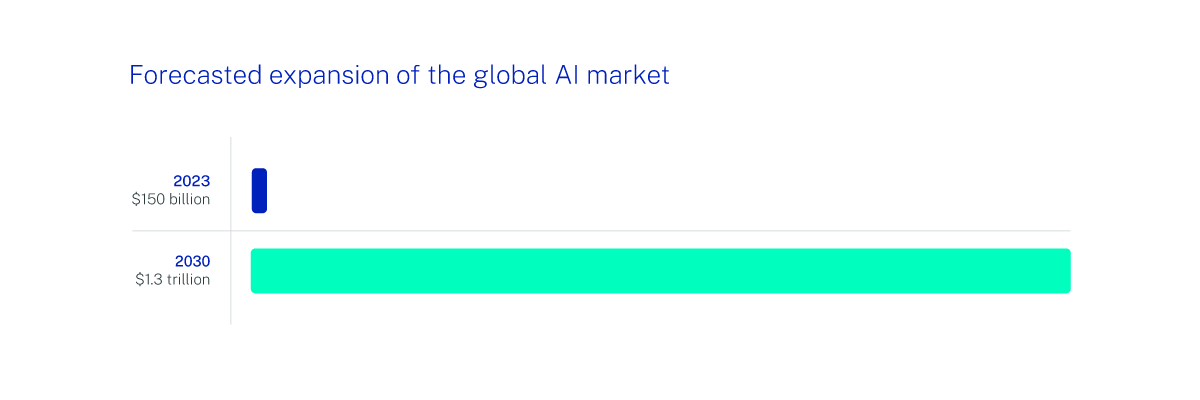

The use of Artificial Intelligence (AI) in finance and just about every other sector you can think of has grown exponentially in the last couple of years. Research & Markets has found that the global AI market will expand from just $150 billion in 2023 to more than $1.3 trillion by the end of the decade.

It’s easy to see why AI is growing so fast: the ability to make day-to-day business processes faster and more efficient, and to make more intelligent and informed decisions, can have a transformative effect on the bottom line. And despite some of the regulatory and ethical concerns that are currently being dealt with, the potential synergy of Artificial Intelligence and finance means that AI is just too big an opportunity to ignore.

In this blog, we’ll investigate how AI is already proving itself a force for good in the finance sector, how it will continue to do so in the future, and how the innovations learned here are spreading to countless other types of business.

It’s easy to see why AI is growing so fast: the ability to make day-to-day business processes faster and more efficient, and to make more intelligent and informed decisions, can have a transformative effect on the bottom line. And despite some of the regulatory and ethical concerns that are currently being dealt with, the potential synergy of Artificial Intelligence and finance means that AI is just too big an opportunity to ignore.

In this blog, we’ll investigate how AI is already proving itself a force for good in the finance sector, how it will continue to do so in the future, and how the innovations learned here are spreading to countless other types of business.

Already, some of the biggest names in the sector like Amazon, Microsoft, SAP and Salesforce are applying AI to their benefit, and the benefit of their customers. By doing so, they’re making their services faster, more efficient, more intuitive and ultimately more profitable. While the scope of applications around Artificial Intelligence and finance is vast, many of the applications we’ve seen so far can be grouped into four main categories:

Already, some of the biggest names in the sector like Amazon, Microsoft, SAP and Salesforce are applying AI to their benefit, and the benefit of their customers. By doing so, they’re making their services faster, more efficient, more intuitive and ultimately more profitable. While the scope of applications around Artificial Intelligence and finance is vast, many of the applications we’ve seen so far can be grouped into four main categories:

This is where large data sets are used to identify patterns and provide insights. This means that traders can make more informed decisions about what to buy and sell, and when, far faster and more effectively than they could relying on human intuition or manual data analysis.

This is where large data sets are used to identify patterns and provide insights. This means that traders can make more informed decisions about what to buy and sell, and when, far faster and more effectively than they could relying on human intuition or manual data analysis.

When human errors with data strike in a healthcare scenario, the consequences for patients and care providers alike can be severe. By turning to AI to take care of key data processes instead, the risk of these errors made can be reduced, while sensitive health records can also be kept more secure.

More directly influencing care is the ability of AI to spot patterns in health data to support more detailed and accurate diagnoses of conditions, and to identify the best course of treatment more rapidly. As an example of what’s possible, IBM Watson has already been able to determine treatment plans for patients based on analysis of both structured and unstructured patient data.

The retail sector was perhaps one of the first to adopt AI in a way that would be used regularly by the consumer. Chatbots and automated customer service platforms driven by conversational AI are now commonplace around the world.

Predicted to become the primary customer service channel for roughly a quarter of organizations by 2027, they help customers get faster responses to queries with less stress involved, and help retailers serve a greater volume of customers without investing in increased headcount.

But behind the scenes, things are already getting much more advanced. Just as banking institutions are using AI to personalize product offers and recommendations, so major retailers are doing exactly the same using buying data, web traffic information and customer sentiment analysis.

Where there may be developments in this sector in the future is in democratizing retailer access to AI technology. At the moment, bigger multinational retailers have the most resources to advance their AI deployments the furthest: smaller, independent retailers need help and more affordable solutions if they’re to be able to compete on a level playing field.

Think of AI for travel and you’ll probably most likely be thinking of driverless transport technologies, but there are many other potential use cases for the sector, too.

For example, many of the same customer-facing applications for the retail sector have also been deployed specifically in travel settings. Smart concierges can improve guest experiences at hotels, fielding queries in real time and supporting the delivery of requests like spa treatment bookings and room service. Hotel chain Hyatt has even been able to deploy AI-powered beds that adjust temperature and firmness, based on a customer’s heart rate and breathing while they sleep.

Manufacturing has probably benefited more than most industries from Artificial Intelligence already. The ability to make manufacturing processes and entire supply chains faster, more efficient, more accurate and more insight-driven can make a fundamental difference to the bottom line.

For example, AI-powered predictive maintenance can help manufacturers maximize machine uptime, by spotting potential problems and allowing them to be rectified before they can have any effect. Robotic Process Automation is also helping improve the consistency of the products being made, and reduce human errors that can fall foul of quality assurance and result in wasted time and resources.

The budgeting and cost-tracking innovations that many finance businesses have explored can also be put to use in a manufacturing setting to good effect.

Discussions about the use of Artificial Intelligence are ongoing, alongside existing regulations around data protection and privacy that are already in place (especially in sectors like financial services). This is where robust data governance practices that ensure the security and integrity of sensitive financial data are so important

Many people still have ethical concerns about how AI is used, whether it’s the use of personal information, worries of AI projecting unfair bias, or fears that AI and automation may render many jobs obsolete. It’s because of these issues that transparency in the use of AI and Large Language Models (LLMs) are vital

Customers are naturally wary about their interactions with AI, especially in finance where highly sensitive information around their financial affairs is involved. Extensive research and user testing can help overcome any concerns, and ensure that the public feels familiar and comfortable with any new AI tools that they’re presented with. This will take place in the context of new legislation being implemented in years to come, such as the European Union’s AI Act.

It’s easy to see why AI is growing so fast: the ability to make day-to-day business processes faster and more efficient, and to make more intelligent and informed decisions, can have a transformative effect on the bottom line. And despite some of the regulatory and ethical concerns that are currently being dealt with, the potential synergy of Artificial Intelligence and finance means that AI is just too big an opportunity to ignore.

In this blog, we’ll investigate how AI is already proving itself a force for good in the finance sector, how it will continue to do so in the future, and how the innovations learned here are spreading to countless other types of business.

The impact of AI in banking and finance

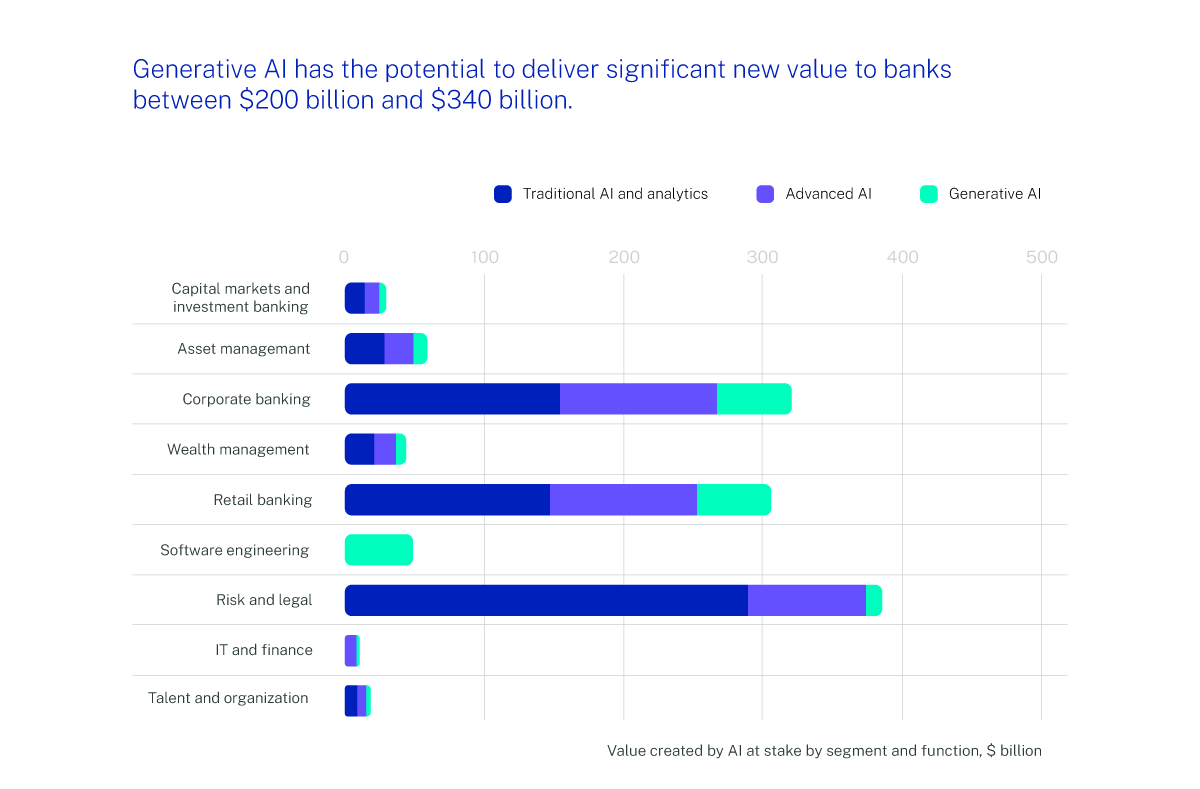

Looking at Artificial Intelligence in finance specifically, Grand View Research has found that the global market was already worth $9.45 billion in 2021 and is expected to grow at 16.5% annually for the rest of the decade. Despite these advancements, a recent Gartner survey revealed that 61% of respondents are not currently utilizing AI, indicating there's room for further adoption and potential growth in integrating AI technologies across the industry. As McKinsey’s latest report points out, the use of AI in banking can bring the most new value to risk and legal departments.

Already, some of the biggest names in the sector like Amazon, Microsoft, SAP and Salesforce are applying AI to their benefit, and the benefit of their customers. By doing so, they’re making their services faster, more efficient, more intuitive and ultimately more profitable. While the scope of applications around Artificial Intelligence and finance is vast, many of the applications we’ve seen so far can be grouped into four main categories:

Identifying fraudulent activity

Cybercrime and fraud is constantly on the rise, with more than 2500 incidents hitting the financial sector in 2021 alone. AI is proving instrumental in helping finance firms (including big hitters like Mastercard) detect fraudulent activity and potential cases of money laundering. Machine learning is increasingly capable in spotting patterns of suspicious transactions, meaning that this kind of criminal activity can be detected, investigated and shut down far more quickly. Fraud and financial misappropriation affects many industries, so it’s clear that the use of AI here can benefit a range of other sectors. For example, the insurance sector can more easily deal with fraudulent claims; the healthcare industry can respond to prescription fraud where medication is dispensed to the wrong people; and local and national governments can more effectively clamp down on tax evasion and benefit fraud. Similarly, we’ve helped the Swedish online betting company Betsson build smarter and more secure payment infrastructure.

Analyzing data sets for trading

In a survey of CFA Institute members, more than half (56%) mentioned their companies regularly use AI and 'big data' for analyzing information. Additionally, a quarter (26%) noted their companies use these technologies to make decisions, and quantitative trading is no exception.

This is where large data sets are used to identify patterns and provide insights. This means that traders can make more informed decisions about what to buy and sell, and when, far faster and more effectively than they could relying on human intuition or manual data analysis.

Budgeting and cost tracking

At a more customer-facing level, AI is helping customers manage their personal finances better, whether it’s advice around financial management, faster and more convenient transactions, or tracking of expenses and savings goals. For example, Capital One is using AI to offer tailored financial advice and product recommendations to its customers, based around their financial history and transaction data. The firm analyzes spending habits, financial goals and overall attitude to risk, and uses this information to connect customers to services and products that are best suited to their specific needs.Product personalization

In every sector that’s consumer-facing, customers are constantly demanding more personalized and intuitive experiences. In the context of the finance and banking industry, this means fast, stress-free responses when customer service or support is required; easy access to key banking services; and the knowledge that their bank is working proactively to keep their data and funds safe. But it can also be used to deliver offers and recommendations to customers, based on insights driven from AI. American Express is already doing this to good effect, including sending customers personalized rewards.What can other industries learn from the adoption of AI?

The finance industry is leading the way in terms of AI, in no small part because of the importance of the money and data involved. As such, the sector is to some extent acting as a bit of a guinea pig for testing out the successes and potential pitfalls of the technology, so that other sectors don’t make the same mistakes on their adoption journeys. For those sectors that are much earlier on in their exploration of AI, this gives them an opportunity to learn from how it’s been applied in finance, and how they can work the same principles into their own operations. Examples of this include: AI in healthcare

AI in healthcare

When human errors with data strike in a healthcare scenario, the consequences for patients and care providers alike can be severe. By turning to AI to take care of key data processes instead, the risk of these errors made can be reduced, while sensitive health records can also be kept more secure.

More directly influencing care is the ability of AI to spot patterns in health data to support more detailed and accurate diagnoses of conditions, and to identify the best course of treatment more rapidly. As an example of what’s possible, IBM Watson has already been able to determine treatment plans for patients based on analysis of both structured and unstructured patient data.

AI in eCommerce

AI in eCommerce

The retail sector was perhaps one of the first to adopt AI in a way that would be used regularly by the consumer. Chatbots and automated customer service platforms driven by conversational AI are now commonplace around the world.

Predicted to become the primary customer service channel for roughly a quarter of organizations by 2027, they help customers get faster responses to queries with less stress involved, and help retailers serve a greater volume of customers without investing in increased headcount.

But behind the scenes, things are already getting much more advanced. Just as banking institutions are using AI to personalize product offers and recommendations, so major retailers are doing exactly the same using buying data, web traffic information and customer sentiment analysis.

Where there may be developments in this sector in the future is in democratizing retailer access to AI technology. At the moment, bigger multinational retailers have the most resources to advance their AI deployments the furthest: smaller, independent retailers need help and more affordable solutions if they’re to be able to compete on a level playing field.

AI for travel

AI for travel

Think of AI for travel and you’ll probably most likely be thinking of driverless transport technologies, but there are many other potential use cases for the sector, too.

For example, many of the same customer-facing applications for the retail sector have also been deployed specifically in travel settings. Smart concierges can improve guest experiences at hotels, fielding queries in real time and supporting the delivery of requests like spa treatment bookings and room service. Hotel chain Hyatt has even been able to deploy AI-powered beds that adjust temperature and firmness, based on a customer’s heart rate and breathing while they sleep.

AI for manufacturing

AI for manufacturing

Manufacturing has probably benefited more than most industries from Artificial Intelligence already. The ability to make manufacturing processes and entire supply chains faster, more efficient, more accurate and more insight-driven can make a fundamental difference to the bottom line.

For example, AI-powered predictive maintenance can help manufacturers maximize machine uptime, by spotting potential problems and allowing them to be rectified before they can have any effect. Robotic Process Automation is also helping improve the consistency of the products being made, and reduce human errors that can fall foul of quality assurance and result in wasted time and resources.

The budgeting and cost-tracking innovations that many finance businesses have explored can also be put to use in a manufacturing setting to good effect.

Is AI inevitable or will some industries avoid it?

As the use of AI in business continues to grow, there will naturally be pressing questions as to the limits of its capabilities. How far can it go? Will every industry become primarily AI-driven? And how many people are at risk of losing their jobs because AI technology can do the work faster, cheaper and more consistently? Well, AI is advancing so quickly that it’s impossible to look too far into the future, and predict with any certainty which sectors definitely will or won’t be transformed by AI. However, there are some places where human endeavor is most likely to win through. For example, while generative AI and large language models like ChatGPT have been able to generate written and visual content, they lack the creativity and originality that only humans can provide because they can only work with the data they’re given. Additionally, concerns around data protection, data security and copyright infringement may limit the scope of tools like this in the years to come. AI ultimately thrives on objectivity: using hard facts and data to come up with information and insights. The flip side of that coin is that anything involving subjectivity will likely remain the primary reserve of human effort, such as interpreting law (the legal sector), building human relationships (politics and public relations), inspiring learning through a human connection (education), and delivering reassurance alongside care (healthcare). Perhaps this is why finance has stood out as a major driver in AI innovation: dealing with the unarguable objectivity of data and numbers is ideal for intelligent automation, as there is very little subjectivity involved.Challenges around AI adoption

AI is still in its relative infancy and there are many hurdles and growing pains that the technology will have to deal with in the months and years to come, such as: Data security and regulation:

Data security and regulation:

Discussions about the use of Artificial Intelligence are ongoing, alongside existing regulations around data protection and privacy that are already in place (especially in sectors like financial services). This is where robust data governance practices that ensure the security and integrity of sensitive financial data are so important

Ethics and bias:

Ethics and bias:

Many people still have ethical concerns about how AI is used, whether it’s the use of personal information, worries of AI projecting unfair bias, or fears that AI and automation may render many jobs obsolete. It’s because of these issues that transparency in the use of AI and Large Language Models (LLMs) are vital

Customer adoption:

Customer adoption:

Customers are naturally wary about their interactions with AI, especially in finance where highly sensitive information around their financial affairs is involved. Extensive research and user testing can help overcome any concerns, and ensure that the public feels familiar and comfortable with any new AI tools that they’re presented with. This will take place in the context of new legislation being implemented in years to come, such as the European Union’s AI Act.

In summary

The good news is that none of these challenges are insurmountable, and the clear benefits of using AI in banking and finance massively outweigh the headwinds that finance firms like you might face along the way. But the easiest way to do so is to partner with an AI expert who not only understands the capabilities of the technology but also how to apply it in the specific context of your business and industry.Working with Ciklum means you get access to leading expertise in the world of AI, a global workforce of developers and solution design experts, and a path towards maximizing the potential of AI for your organization. To learn more about our services for Artificial Intelligence in finance, get in touch with us today for an informal, no-obligation chat.

By Ciklum Editorial Team

Ciklum’s Editorial Board is a collective of experienced writers and industry experts, bringing together perspectives shaped by real-world engineering and delivery experience. Through collaborative insights, the team explores how technology, AI, and digital innovation move from concept to execution across industries.

Blogs

Discover Similar Insights

The AI Readiness Gap: 5 Blockers Causing Most AI Failures

Learn More

The $17B Contact Centre Opportunity: 5 Conversational AI Trends Reshaping UK CCaaS

Learn More

The Agentic SDLC: How AI Is Rewiring Software Development In 2026

Learn More

Why Enterprise AI Projects Fail: The Misallocation Problem Costing Millions in 2026

Learn More